Download Macroeconomics: Understanding Business Cycles, Inflation, and Unemployment and more Study notes Macroeconomics in PDF only on Docsity!

is What

- 4 Macroeconomics of Overview 1. Macroeconomics? - 5 Macroeconomic Concepts 1. - 5 Output and Income 1.2. - 5 Unemployment 1.2. - 8 Distribution Income and Production of Factors 1.2. - 8 Inflation 1.2. - 10 Economy Real Markets and the Financial 1.2. - 11 Openness 1.2.

- 12 : Economic Growth Run Long the Macroeconomics in 1.

- 13 Cycles Business Run: Short the Macroeconomics in 1. - 15 cs Macroeconom i of Genesis The 1.5. 15 ceien Sc a as Macroeconomics 1.s - 18 Macroeconomics and Microeconomics 1.5. - 20 Supply Demand and 1.5. - 21 Macroeconomics of Methodology The 1. - 21 Explained? to be is What 1.6. - 21 Realism Theory and 1.6. - 22 Analysis and Normative Positive .6.3 - 22 Data of Role The ories:The Testing 1.6. - 22 and Forecasting Modelling Macroeconomic 1.6. - 24 Book the of Preview 1. - 24 re Structu 1.7. - 24 Intuition Rigour and 1.7. 24 Controversies and Consensus 2 1.7. - 24 Institutions and Data 1.7. - 25 Europe 1.7.

4 PART I I NTRODUCTION TO MACROECONOMICS

The Theory of Economics does not furnish a body of settled conclusions immediately applicable to policy. It is a method rather than a doctrine, an apparatus of the

mind, a technique of thinking, which helps its possessor to draw correct conclusions. ]. M. Keynes

Overview of Macroeconomics

Unemployment, inflation, booms and busts, finan- cial markets, interest rates, and exchange rates are everyday fare in the news. All these phenomena affect our well-being. This why macroeconomics is so exciting. Macroeconomics is more than just head- lines, however: it is a fascinating intellectual adven- ture. The breadth of issues it covers is evidence enough of its inherent complexity. Yet, a few sim- ple ideas can go a long way seeing through com- plex situations. Macroeconomics is also enormously useful. People, rich or poor, are affected as jobs appear or vanish and as prices change. Businesses can gain or lose large amounts of money when their environment changes, regardless of how well they are managed. Citizens want to understand what their governments are up to. Dramatic events like depressions, when overall economic activity is very far below average and unemployment soars, or hyperinflations, when prices are increasing at monthly rates of 50% or more, can tear at a soci- ety's social fabric, and yet can be prevented when policy-makers apply sound economic principles. But are 'sound economic principles' valid? The events that started in 2007 and led to the Great Recession and the Eurozone crises have led some observers to conclude that macroeconomics needs to be overhauled. Yet it is also common to blame medical doctors for epidemics, and or messengers for bringing bad news, and that doesn't sound fair. Macroeconomists are in a similar situation today. We will argue that macroeconomics as a field has proved its mettle. To be sure, our understanding is very far from perfect. In particular, macroecono- mists are not good at making forecasts and the pro - fession has failed to see the crisis coming. Yet , the principles underlying our field made it possible to understand these dramatic events surprisingly well

as they unfolded. They also contained prescriptions for what needed to be done. When governments heeded this advice, the economic situation in fact improved. In any case, we did not experience the Great Depression of the 1930s, and we know why. Besides helping diagnose such situations, the mate- rial in this book will teach you humility: Some events, both economic and political, cannot be pre- dicted. This includes banking and financial crises, which contain strong behavioural elements. A key feature of macroeconomics is that it is geared to finding solutions. Its principles may look abstract at first, but they readily lead to policy pre- scriptions. These prescriptions are directly related to the observation of economic events with unde- sirable consequences, which in turn presumes agreement on what is to be measured and how measurements are made. Before the arrival of macro- economics, concepts such the gross domestic product (GDP), the consumer price index, or the unemployment rate simply did not exist. Some of these concepts are presented in Section 1.2, many more will be introduced as we move through the book. The next step is to formulate a diagnosis. A key challenge at this stage is to distinguished between business cycles, or short-run fluctuations of output and employment, and long-run trends. This distinction, which is presented in Sections 1.3 and 1.4, shapes the structure of the book; both repre- sent the subject of macroeconomics and the objec- tive of macroeconomic policies. Equipped with these preliminary essentials, we can then examine in what sense macroeconomics is a science (Section 1.5) and how it helps us to reason about the world around us (Section 1.6). The chapter con- cludes with a preview of the book's contents (Section 1.7).

6 PART I INTRODUCTION TO MACROECONOMICS

,, Real Income per Capita (GDP in euros, 2000 prices) ~o /) -

1900 1913 1929 1950 1987 1992 1999 2002 2007 201 O 2015 Av. growth rate

Aust ria 2.462 2,961 3, 160 3, 167 13,085 14,937 17, 145 17,920 20,289 20,280 20,824 1.9% Bel gium 3, 188 3,606 4,3 19 4,667 13,280 15,078 17,010 17,987 20,069 20,071 20, 104 1.6% Den mark 2,578 3,343 4,337 5,933 15.401 16, 192 19,017 19,717 21.414 20,346 20,552 1.8% Finl and 1.426 1,804 2,322 3,634 13.144 1 2,837 15,931 17, 152 21,051 20,008 19,582 2.3% France 2.457 2,978 4,025 4,504 14, 144 15.774 17,549 18,61 O 19,040 18,562 18,904 1.8% Germany 2,550 3, 117 3.462 3,316 13.417 14.433 15.737 16,399 18,066 18,018 19.420 1.8% Italy 1 ,526 2, 191 2,643 2,992 12,771 14,216 15,612 16,339 17,229 16,329 15,330 2.0% Netherlands 2,925 3,459 4,861 5, 124 13.447 15, 165 17,966 18.493 20,854 20,489 20,715 1.7% Norway 1,604 2,091 2,895 4,639 15,521 16,715 21,019 22,093 24,399 24,096 24,714 2.4% Sweden 2,188 2,646 3,306 5.759 14.483 14,509 16,962 18, 144 21,688 21,192 22,285 2.1% Switzerland 3,275 3,645 5,410 7.745 16,912 17,800 18,590 19, 179 21, 175 21,534 21,944 1.7% United Kingdom Canada

3,838 4,205 4,703 5,930 13, 154 13,785 16,650 1 7,8 17 20, 183 19, 158 20,311 1.5% 2.488 3,800 4,328 6,231 15,678 15,511 18,347 19,654 21,619 21,292 22,446 1.9% USA 3,496 4,529 5,895 8, 170 18,618 19,908 23,669 24,383 27,052 26,348 28,065 1.8% Argentina Bangladesh China

2,355 3,245 3.732 4,261 6,237 6.406 7,443 6,083 8,803 9.310 10,069 1.4% 1.1% 2.6% 1.7% 2.6%

417 466 512

443 472 575

445 481

461 515 574 708 778 960 1,088 1, 383 1.484 1,822 2.702 3,586 4,857 6,299 8, India (^622 529 961) 1,146 1,568 1.719 2,402 2,847 3, Japan (^) 1,008 1, 185 1,731 1,641 13,887 16,648 17,597 17,918 19,505 19,005 19,

Source: www.eco.rug.nl/-Maddison/and The Conference Board and Groningen Growth and Development Centre, Total Economy Database, January 2011, http}/www.conference-board.org/economics/The Maddison-Project, http}/www.ggdc.net/maddison/maddison-project/home.htm, 2013 version. IMF, World Economic Outlook Database April 2016.

There are many reasons to be concerned about unemployment. A first reaction to the image of idle workers is one oflost production and income. At the same time, we need to ask whether the unemployed are able to find offers of work, whether they are turning down job offers, and if so, for what reason. Are the jobs that workers are searching at all, or are workers really unavailable for jobs on offer, perhaps because their expecta- tions are unreasonable? Or are they simply frus- trated not to find a job and have given up looking?

Unemployment is generally not a pleasant affair. Even with well-developed and efficient unemploy- ment assistance programmes, long-term jobless workers can experience emotional stress and their skills may deteriorate. Even if they are not measur- able, the social and psychological costs of unem- ployment are high for the affected individuals and for society as a whole. By that criterion, Europe has not done well over the last decades , as Figure 1. shows. The average rate of unemployment has grown inexorably to reach double-digit numbers. In the USA, in contrast, unemployment has closely

8

'Denmark

e Switzerland

Finl!wJ!,ve~er,

•Norway

Cw;ta (^) Rica

••

: Aus (^) ra (^) 1a

United

(^) States

uo~•

U~d (^) Kingd~,Keland

Pallu

United

(^) Arab Emirates

Luxembourg

•Germany

•Singapore

7

.• (^) Argenti<j

•France

Qatar•

•• •Suriname

1# (^) Spa in

Saudi (^) Arabia

•Taiwan

_ •Guatemala

Trinidad and Tobago

.!!! · (^13) 0 c (^6)

l~icara~a

=

= JU,..UO

e L1ty~

~ (^) ~olaid

'

Russ1ae

(^) Cyprus

•Estonia

e

Bh'ii!n

Turkey

I

•-Phi

lin

!~~gina•

•Portuga

(^) l

e -

!I' ";'")Wlnia

e

ongelia

e• (^) Greece

·~ 5

:.::; J!' Vl

9'~i'a~a~r•n•

~q

e j'b9'lic;eorg1a

(^) •

Egypt (^) • (^) Bulgaria

.. ..

~ger

Gabon

4 ~-~had A ghanistan

•Benin^ •Rwanda

3 'Togo 02

20000

40000

~anra1n e Hong (^) Kong (^) SAR

60000

•Kuwait

80000

GDP (^) per (^) cap ita in (^2014) (^) International

(^) Dollars

(^) {from (^) IMF (^) WEO)

Fig. (^) 1.

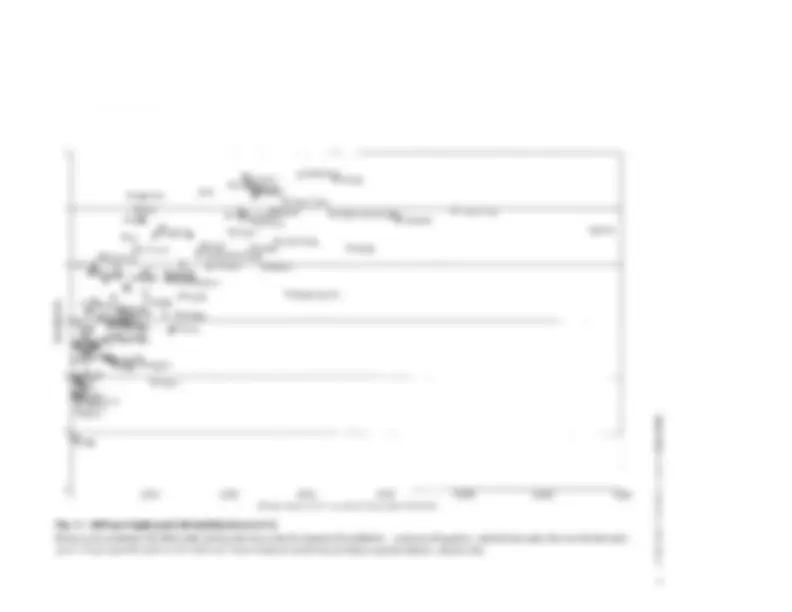

GDP per

(^) Capita

(^) and Life Satisfaction

(^) in (^2014)

100000

(^120000)

140 000

Money

(^) is (^) not (^) everything in life.

(^) While

(^) public

(^) opinion

(^) polls (^) show a

(^) clear (^) link (^) between

(^) life (^) sat (^) isfaction-a

(^) measure

(^) of (^) happiness-and

(^) GDP (^) per capita,

(^) that (^) link (^) is (^) far from tight.

Sources:

(^) GDP (^) per capita from

(^) World

(^) Economic

(^) Outlook,

(^) IMF; (^) Ind ex (^) of (^) satisfaction with

(^) life: (^) http ://en.wikipedia.org

/w iki/Sati

sfac tion_with_Life_lndex

'-l ·~ <.n n s: 0 z 0 n m 0 :xJ n)> s: <.n --i )> :r: ~ ;JO m-i .,, J> ::c n

80 8S

0 c:- 7S

~ l?

~ (^70) ~ 6S

France

~

~-

(^160) Q) SS

3SO

8S

300 (^) -

80

0 0

c:-

2SO (^) J\

(^0) 7S

l?

0

200 (^) ~

~ (^) 70

u Q)

Q)

lSO (^) - (^) ~

~ 6S

-"'

~

u

Q)

100

g

160

Q)""iii

so

SS

~

0

Denmark

300 3SO 00 -

2SO "' "'^ J\

200 u ~^ c

lSO u^ -"'^ ·~

100

Q)^ ""iii^ g

so "'

(^1) 9SO (^1) (^) 9SS (^) 1960 196S 1970 197S 1980 198S 1990 199S

(^2000) (^) 200S (^2010) (^) 201S

(^1) 9S (^1) 961 (^1966)

(^1971) (^) 1976 1

98 (^) 1 1986

(^1991) (^1996)

(^2001) (^2006) (^2011)

I- Labour

(^) Share%

(^) of (^) GDP (^) at (^) Factor

(^) Cost (^) -

Re (^) al (^) Stock (^) Pric (^) es (^) 199S=

(^) I

Netherlands

8S

3SO

80

8 c:- (^) 7S

~ 0 ~ (^70) ~ 6S

~ Q) (^60)

3: SS

300 00

2S (^) O "' "'^ J\

200 u Q)^ ~

lSO u^ -"'^ ·~

100 Q)^ ""iii^ g

so "'

~

0

19Sl (^) 19S6 1

961 (^) 1966 1971 1976

(^1981) (^1986)

(^1991) (^1996) (^2001) (^2006) (^2011) (^2016)

I-

Labo ur (^) Share %

(^) of (^) GDP (^) at (^) Factor

(^) Cost (^) -

Real (^) Stock (^) Prices (^) 199S=lO

(^) OI

(^1) -- (^) Labour Share %

(^) of (^) GDP (^) at (^) Fa c tor (^) Cost (^) -- (^) Real (^) Stock (^) Prices

(^) 199S=

100 (^) f

Sweden

8S

3S (^) O

80

8 c:- (^) 7S

~ 0 ~ (^70) ~ 6S

~ Q) 60

3: SS

19S (^1961) (^1966) (^1971) (^1976)

(^1981) (^1986)

(^1991) (^1996)

(^2001) (^2006) (^2011)

(^1) -- (^) L abour (^) Sha r (^) e% (^) of (^) GDP (^) at Factor

(^) Cost (^) -- (^) Rea (^) l (^) Stock

(^) Prices (^) 1995=

100 (^) I 300

g

2SO "' "'^ J\

200 u Q)^ ~

lSO u^ -"'^ -^ ~

100 Q)^ ""iii^ g

so "'

Fig. 1.

(^) Labour Share

(^) of (^) Income

(^) in Manufacturing and Stock Prices, Four Countries,

(^) 1950-

Labour and

(^) capital

(^) share the fruits

(^) of (^) the economic

(^) ac tivit y. Th (^) e labour

(^) share is the fraction

(^) of (^) econom ic

(^) output

(^) which

(^) is (^) paid (^) to (^) workers in wages and other forms

(^) of

compensation.

(^) Th e valuation

(^) of companies, reflected in stock prices,

(^) is (^) negatively

(^) associated wi

th (^) the (^) labour

(^) share.

(^) Real (^) stock prices

(^) are (^) computed

(^) as (^) a share price index

divided by the

(^) GDP (^) deflator, a measure

(^) of (^) the price

(^) level.

Sources:

(^) Labour share:

(^) AMECO

(^) database, European Commission; Stock prices:

(^) Economic

(^) Outlook,

(^) OECD.

\D "'·~ n s: 0 z 0 n m 0 :0 n)> s: ~ :r: ~ :i:i m -I "'~ :r n

10 PART I IN TR OD UC TION TO MA CROECONO MICS

cent were quite common in the 1980s. When inflation is very high it is usually measured on a monthly basis; the term hyperinflation describes situations when this monthly inflation rate exceeds 50%. A sign of exceptional economic dis- tress, hyperinflation has been observed in Central Europe in the early 1920s, in Latin America in the 1980s, and in many countries which emerged from the collapse of the Soviet Union in the early 1990s. In normal times, inflation is related to the business cycle. Figure 1.4 shows how the rate of inflation changes when the rate of capacity utili- zation varies. The rate of capacity utilization measures the degree to which companies are truly employing their available plant and equip- ment, and it serves as a good indicator of cyclical conditions. The inflation rate is generally procy- cl ic al: it tends to rise when activity is high and declines in periods of slack. In contrast, the unemployment rate is countercyclical : it moves

5 4

E" 3

"c: c:

"'^2

w0..

~c: (^0) 0 ·~ 0:: .!O -

.!O .,

QI) c: -

..c:u "' -

against the cyclical behaviour of output, falling when output is growing rapidly and rising when output is growing more slowly or falling. The behaviour of inflation is investigated in Parts III and IV of this book.

1.2.5 Financial Markets and the Real Economy Financial markets play a central role in modern economies. Either literally or with the help of sophisticated communications technologies , they represent arenas where buyer s and sellers of finan- cial assets such as bonds, stocks, currencies, and other financial instruments meet to trade. Together with banks and other financial institutions, finan- cial markets gather resources from households and firms in the form of savings and lend them out to others who will spend them. One specific fea- ture of these markets is the extreme day-to-day variability of prices at which financial instruments are traded.

90

85

80 E"

"c: c:

"'w

75 0.. ~

·^ c c;

u"'

65

1967 1971 1975 1979 1983 1987 1991 1995 1999 2003 2007 2011 2015 -- Change in inflation {left axi s) -- Capaci ty utilization rate (right axi s)

Fig. 1.4 Capacity Utilization Rates and Changes in Inflation Rates, USA, 1967-201 S When measures of the utilization of capacity indicate a high level of activity in factories, the rate of inflation tends to rise, i.e. prices rise at an increasing rate. Conversely, low levels of activity are accompanied by declining rates of inflation. Sources: Bureau of Labor Statistics (CPI ) and Federal Reserve Bank of Saint Louis (capacity utilization).

12 PART I IN TRODUCTION TO MACROECONOMICS

Macroeconomics in the Long Run:

Economic Growth

Figure 1.S(a) displays estimates of GDP for France, Germany, and the UK since 1870. A positive long-run general tendency, or trend, clearly dominates shorter- run fluctuations. The trend rate of growth has been fairly stable, perhaps with a sli g ht increase after the

Second World War. Another way of seeing this is to plot th e natural lo gar ithm of GDP against time, as in panel (b) of Figure 1.5. With this so-called logarithmic scale the slope of the curve is a direct measure of the annual growth rate: a constant growth rate would

~

e

0 "<lJ

(^00) N (^0) ~ c ~ cc

(a) 1800 1600 1400 1200 1000 800 600 400 200 0

{b)

1 -- France -- Germany -- United Kingdom I

o~o~o~o~o~o~o~o~o~o~o~o~o~o~o~ oooooo ~~ NNMM~v~~~~~~oooo~~oo ~~ 000000000000~~~~~~~~~~~~~~~~~~~~0000 ~~~~~~~~~~~~~~~~~~~~ ~~~~ ~~ NNNN

7.5 ~---------------------------~ E I-- Fr ance -- Germany -- United Kingdom I £ 7

e

"<lJ^5 (^80) ~ 4. 4

o~o~o~o~o~o~o~o~o~o~o~o~o~o~o~ oooooo ~~ NNmmv~~~~~~~oooo~~oo ~~ 000000000000~~~~~~~~~~~~~~~~~~~~0000 ~~~~~~~~~~~~~ ~ ~~~~~~~~~~~~ NNNN

Fig. 1.5 Gross Domestic Product (GDP), France, Germany, and the UK, 1870- Nation al output and income, as captured by the gross domestic product, exhibits a robust growth trend. Growth tends to be expon ent ial; that is, annual percentage increases are reasonably stable in the long run. This does not preclude significant year- to-year variations (panel a). When the data are displayed on a logarithmic scale instead (panel b), the slope of the curve measures the annua l rate of growth. So urce: 1870- 1949: Maddison ( 1991 ) (http :// www.ggd c. ne t/ maddi so n/ oriindex.htm); 1950-2015: Conference Board's Total Economy Databa se (https:// www .conference-board.org/data/ economydatabase/ index.cfm?id =27762).

long run, on average, we the In 4 yield a straight line.

seem very close to a rather robust and steady trend.

implies remark- output total in growth trend This

another living standards. Let's take in able increases

average, or capita, per that Note 1. Table 1. at look

Belgium in sixfold than more income increased to

in 18-fold and Sweden, in ninefold 1900, since

shared not is phenomenon growth the Yet Japan.

all times. In Bangladesh, real at all countries by

same the over 120% capita rose by only per income

countries have faced serious setbacks, Some period.

have others while famines, and wars as such

and India, stag- China expanded rapidly. Some, like

decades before suddenly entering a many nated for

China rapid increase in living standards. of period

13 IC57 MACROECONOM IS WHAT 1 CHAPTER

stan- in increases momentous these of Because

most the of one is economic growth living, of dards

3 Chapter macroeconomics. in issues exciting

economies why reasons the detail in explores

population, in increase an is reason One grow.

more produce and work can people more since

of means of accumulation the is Another output.

roads, commu- equipment, and plant production:

infrastruc- of forms other and nication networks,

productive. Most impor- more workers make ture

of harnessing and development the is tant

economic ends. The to technology and knowledge

scientific discoveries towards of sharp acceleration

to thought is century eighteenth the of end the

some and industrial revolution, the have triggered

new a of onset the witnessing now believe we are poses a particularly interesting case because its

tele- and advances related to information of wave because it was and explosive take-off was so recent,

communications technology. years ago. 700 advanced economy most world's the

Cycles Business Run: the Short in Macroeconomics 1.

have increased by stag- income and output While

not is growth decades, many over amounts gering

that steady. Figure 1.5 shows even or constant

its trend. around fluctuate to tends output real

which Figure 1.6, in apparent more even This is

the for GDP in change of rate quarterly the plots

relative the accentuate to tend Quarterly data UK.

fluctuations. These sus- short-run of importance

downs are called busi- and ups of periods tained

macro- of challenge important One ness cycles.

GDP of deviations such explain to economics is

out- the as to referred trend, underlying its from

per- and fluctuations occur these do Why gap. put

years, 10 to three from ranging sist over periods

the avoid to anything, if be done, can what and

is This them? with associated are that disruptions

this of IV and III Parts of theme common the

. book

at x of e valueth x(t), if matically inclined readers, atheFor m 4

en th as (1/x)dx/dt, defined g, rate constant grows at t, time

+ gt. O)x( ln = )x(t ln and x(O)egt = x(t)

While business cycles are hardly identical across

of number countries and across time, they have a

features. These features are represented in common

The idea is simple. Imagine Burns-Mitchell diagrams.

a curve like those depicted in Figures 1.5 up cutting

superposing all these and cycles of 1.6 into a set or

necessary is it do this, To each other. of cycles on top

points turning to identify calendar dates for cyclical

with we will be concerned (GDP)-here output of

procedure can be used for troughs as the but peaks,

well. Having identified those cyclical peaks, simple

macroeconomic vari- other of numerical averages

calen- the interest can be calculated around of ables

of output's peak. The behaviour the of dar date

output of points turning the those variables around

variables are the whether tells us something about

forecast help can they that leading-meaning

output. More importantly, in points turning future

theories of formulation the can help inform they

business how understand better which will help us

provides 1.1 Box cycles arise and develop over time.

Burns-Mitchell methodology. the on details more

15 MACRO ECONOMICS? IS W HAT 1 CHAPTER

(Continued) and Then Now Diagrams, Burns-Mitchell

The 5 data. quarterly of years 35 economies over about

panel which appears in the first cycle a reference is result

identified by this procedure are cycles The 1.7. Figure of

which 1.7, Figure of panels other produce the to used

O 1 qua rters before and 10 variables of give the behaviour

stated in propor- usual ly peak, cyclical the quarters after

1.8, reu Fig In period. that over value the average to tion

Mitchell, Burns and of findings original we present the

late data from the US monthly primarily worked on who

twentieth century. early the especially nineteenth and

a Science as Macroeconomics 1.s

Macroeconomics of The Genesis 1.5.

and fluctuations-ups do we observe cyclical Why

Why its trend? around GDP of level the downs-in

generally countercyclical, while unemployment is

inflation appear procyclical? For a long in changes

such phe- to attention time, economists paid little

ft.mc- properly that In fact, it was believed a. nomen

possible best the would deliver markets tioning

at a good approximation to collective outcome,

looking into in point no was there that and least,

called was principle This behaviour. aggregate

laissez-faire endorsed of Opponents 'laissez-faire'.

sup- government interventionism- of some form

and industries, includ- markets for particular port

foreign from protection and subsidies ing

competition.

were cycles business that mean not does This

varying of cycles fact, In completely. ignored

studied, ranging from and lengths were identified

two years' duration to or one of inventory cycles

1.2 pro- Box a century. half long-wave cycles lasting

these cyclical movements. Such on vides details

outcomes cumulative the as seen were cycles

and can be (2001) Pagan due to Harding and is The method 5

of moving average four-quarter follows. For a as ized ar mmsu

quarter for which the as original series, define a peak the

two successive the the two preceding and than higher is GDP

more consecutive peaks are found , or quarters. In case two

retained. Next examine the highest and is highest the only

peaks. Now repeat the of lowest points in a neighbourhood

discoveries, inventions, as such disturbances of

bad crops, wrong bets by or exceptionally good

even or to buy, want customers that goods on firms

abroad. and e hom at consumers of changing tastes

rapidly of consequence the as Inflation was seen

gold discov- of growing money stocks, first because

century, afterwards because nineteenth the in eries

creation by central banks. money reckless paper of

this wisdom of much 16, Chapter in will be seen As

of Great Depression the Yet remains valid today.

and world the throughout 1930s, which spread the

misery, and unemployment into millions sent

seemed too severe to be simply bad luck. Reflecting

1936, British econo- in Great Depression the upon

General The Maynard Keynes published John mist

that a book Money, and t es Inter Employment, of Theory

macroeco- of field the often said to have started is

aggregate of role the stressed Keynes nomics.

fol- His macroeconomic fluctuations. in demand

in lowers later persuaded policy-makers to engage

manipu- to is, that ement,ag man aggregate demand

out smooth to order in demand government late

fluctuations , mainly to avoid protracted recessions.

m movinger unweighted short-t an using re procedu the

these of e neighbourhood th e original series. Inth of average

intermediate turning points, troughs and peaks are

a set ss ese path If. es unsmoothed time seri the determined in

the of magnitude the on additional restrictions of

l turning ca li e final cyc th as fluctuation, they are selected

points.

16 PART I I NTRODUCTIO N TO MACRO ECONOM I CS

Real GDP Q)^ 1, OD ~ Q) ~^1 , t:'.^ ~

"':::^ 1,

'! ;::; (^2) Q) (^) 0, ·~^ > ~ Q) 0, ::: ~ 0,

- 10 -5 0 5 10 Quarter relative to peak

Unemployment Q)^ 1, OD ~ Q)> 1, "'~ Q) t:'.

"':::^ 1,

;::;^ '! (^2) Q) (^) 1, ·~^ > ~Q) (^) 0, ::: ~ -5 0 10 Quarter relative to peak Short term interest rate Q)^ 1, OD ~ Q) >^ 1,

"'~ Q) 1,

t:'.

;::; 1, (^2) Q) (^) 0,

~ (^) 0, ~ Q) ::: 0, ~ -5 0 10 Quarter relative to peak

Q) ~ ~ 2, Q) t:'. "'?- 1, ;::; ~ 0, ·~^ > ~ Q) -1 (^) ' 00 ::: ~

Real GDP (growth rate)

-2,00 ~-~-~-~~ -10 -5 0 10 Quarter relative to peak Price inflation Q)^ 1, OD ~ Q)> (^) 1,

t:'. (^) 1,

;::;^ '! 1, (^2) Q) ·~>^ 0, ~ Q) 0, ::: ~ -5 (^0 5 ) Quarter relative to peak Total employment Q)^ 1, OD ~ 1 ,

"' ~ 1 ,0^1

t:'.

'! ;::; 1, (^2 1) ,

·~^ "'>

~ 0,

~ -5 (^0 ) Quarter relati ve to peak

Fig. 1.7 Burns-Mitchell, Now: Eight Countries, 1970- These six figures display the average behaviour of variables around cyclical peaks, where the cycle is measured using a procedure described in the text. The vertical line around zero shows the quarter in which real GDP reaches its peak (upper left panel). The peak is followed on average by a sharp drop in the growth rate of output (upper right panel). Unemployment is countercyclical, rising most after the peak in GDP has been passed, but is rising across cycles, indicating that average unemployment rates in the sample were increasing over time. The inflation rate is procyclical but lagging, peaking in the quarter after output. Short-term interest rates and employment are strong ly procyclical. Source: OECD; authors' calcu lation s.

18 PART I INTRODUCTION TO MACROECONOMICS

An evaluation of the success of demand man- agement policies is presented in Chapters 16 and

- Since the Second World War, the amplitude of the business cycle appears to have diminished considerably, as can be seen in Figure 1.5. Of course, the global recession of 2008-2009, some- times called the 'Great Recession', is a major set- back. For centuries, earlier generations assumed that favourable periods of growth were inevitably followed by periods of declining activity. Following Keynes, concern initially centred on fluctuating demand. The attention then turned toward the supply side -m eaning the productive capacity of an economy- and the efficient utilization of labour and capital resources. This applies espe- cially to unemployment, which remains a big problem in much of Europe. These topics are the subject of Chapter 18. Another remarkable change in the behaviour of the post-war economy concerns the general price level, or the cost of goods in terms of money. Until the First World War, prices were as likely to rise as they were to fall, as can be seen from Figure 1.9. Apart from war periods, the price level was trend- less; over long periods of 20 to 50 years, the consumer price index-a measure of the average price leve l-wa s remarkab ly stable. One interpreta- tion of the post-war era-a controversial one, as we

All Kinds of Cycles

shall see-is that macroeconomics has led to more steady output growth at the cost of inflation. In the mid-1980s, concern with high inflation triggered a change of heart. In particular, most central banks have toned down demand management policies and refocused their energy on keeping inflation low. The crisis that started in 2007 is now forcing central banks to recognize that they have a broader duty than price stability; in particular, they have to be concerned with financial stability and the health of the banking system.

1.5.2 Macroeconomics and Microeconomics The macroeconomy is just the sum of hundreds or thousands of markets, each of which is explained by microeconomic principles. Microeconomics is devoted to the study of prices of individual goods and of the markets where these goods are produced and sold. Why do we need two separate disciplines? To a great extent they are linked. Microeconomics is dedicated to the analysis of market behaviour of individuals. Macroeconomics is concerned with collective behaviour, the outcome of individual decisions taken without full knowledge of what others do. Thus macroeconomics should be built on micro- economic principles. This is how the field has

Business cycles, like comets, bear the names of their dis- human births, deaths, and marriages before turning his coverers. Simon Kuznets (1901-1985) was a Russian- skills to interest rates and credit conditions. These Juglar born US economist who received a Nobel Prize for his work on growth. Russian economist Nikolai Kondratieff (1892-1938) developed his theory of long-wave cycles in the 1920s before he was arrested and disappeared; the official Soviet Encyclopaedia then wrote about his work: 'this theory is wrong and reactionary'. It was also in the 1920s that Joseph Kitchin (1861-1932), a South African

cycles -whic h involve fluctuations of investment spend- ing, GNP, inflation, and unemployment-are perhaps the closest thing to the business cycle that we will study in th is book. Interestingly, one of the most robust and regular cycles in economic activity is the cycle that coincides with the seasons of the year. Movements of output in agriculture, statistician and gold trader, uncovered his own more manufacturing, construction, and tourism have obvious rapid cycles of 2-4 years' periodicity, which are associ- ated with inventory movements, bank clearings, and wholesale prices. Clement Juglar (1819-1905), a nine- teenth-century French physician, first studied cycles in

seasonal components which sometimes swamp business cycle fluctuations in magnitude, as do patterns in overall output associated with bank holidays, summer and win- ter weather, and harvest s.

g

'iia

U">

"'OJ

]

~

=

19 MACROECONOMICS7 IS WHAT 1 CHAPTER

levels Price (a)

10000.-~~~~~~~~~~~~~~~~~~~~~~~~~~~---,

France - -

Kingdom United --

1000

100

10 Qi

.,. u^ ·c

c..

:::> E

c^ c

"'~^ .,

0..

~ c^0

·~

c 0::

'--~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ 0. I.() .-^ O .-- U""Io o^ *0*^ *0*^ Ll"'lOl.rlOco co^ r--..^ r--..^ \D^ \D^ U")QLl)QLl)QLI) ui^ L/'lO ~^ -q-^ Ll)Qrn rn^ N^ N^ .--^ r-^ LJ'"lOLJ'"lOUIOo o^ *0*^ OLJ'"lO°' t.nco co^ r--.^ Ot.nO^ r--..

0 N^0 N^0 N^0 *N 0\ 0\ 0\ 0\ 0\ 0\ 0\ 0* 0\ 0\ 0\ 0\ 0\ 0\ 0\ 0\ 0\ 0\ °' 0\ co 00 00 co 00 co

rates Inflation (b)

France --^ %^60 % 50 Kingdom United -- % 40 % 30 % 20 % 10 ### j _,h "::!'A r-~ l~c».11= ~ 1 % 0 % - % - **LI) 0 Lt') 0 LJ'"l 0 Lf)** **_0_** **L/)** **_0_** **LJ1 0 l/) 0 I.I) 0 I.Ji 0 LI) 0 LJ) 0 U1 0 Lf'I 0 LI) 0 tJ')** L-~~~~~~~~~~~~~~~~~~~~~~~~~~~~~_J (^) (^0) % - **r- r- 0 00000 0\0\ 0\0\ CO0\ 00 0\ I""--0\ f""-.0\**^ **_\D_** **0\**^ **_\D_** **0\ ll"I0\ U"'I0\**^ ~ **0\**^ ~ **0\**^ **M0\**^ **M0\**^ **N0\**^ **N0\ .--0\ r-0\**^0 0 **0\ 0\ 00 00 I' f".**^ **C000000000000\0\** **N N N N** **1870-2015 UK, Rates, France and the Inflation Fig. 1.9 Price Levels and** zero on average. Since the to close was stable, and inflation was level the price War, World the First of the outbreak Until of and much 1970s late the been positive, high in has average inflation secularly, risen has level the price War, World Second Os. 201 zero, in the to close low, the 1980s, declining over the 1990s and becoming very . OECD (1991 ); Maddison _Source:_ wever, Ho ee decades.hr t past the evolved over one into markets all together g brin to seeking challenge. In this book, daunting a is framework microeconomic the way. We recall the lf we go ha deci- nd a underst to needed are that es principl invest- productive nd a consumption like sions of importance overriding the , as well as nt m e on insist not do we Yet, constraints. budget 21 MACROECONOMICS? IS WHAT 1 **CHAPTER** ## Macroeconomics of The Methodology 1. **Explained? be to is What .1 1.** aggregate activ- with concerned is Macroeconomics rates, infla- interest unemployment, of level the ity, in trade the and exchange rate, the tion, wages, countries. other with goods , services and assets about these questions, it think Before beginning to to want we what essential to be clear about is the outside or we take as given, what explain and analysis. The variables to be explained of realm **endogenous** using economic principles are called try not we do variables-those other variables. The variables. This dis- **exogenous** called explain-are to of Examples 1.10. represented in Figure is tinction variables often considered exogenous are policy poli- monetary and fiscal of (the tools instruments of cies), economic conditions abroad (foreign levels and oil, of price the interest rates), and activity sometimes even domestic social conditions such as militancy. union trade or business optimism The distinction between endogenous and exoge- necessarily arbitrary. Many exoge- is nous variables the of strictly independent not nous variables are the book progresses in fact, endogenous variables. In steps. Many variables initially are considered exoge- """ variables Exogenous **t** variables Endogenous **Endogenous and Exogenous 1.10 Fig.** **Variables** an in analysis of are the object variables Endogenous are determined variables Exogenous model. economic political The weather and model. outside the economic considered generally variables of examples decisions are be exogenous. to progressively made endogenous, or then nous and endogenized. For example, fiscal and monetary pol- of icy decisions are often responses to the course convenient to is inflation or unemployment. While it sometimes is exogenous, it as regard policy variables these how understand to useful and interesting For exogenous variables themselves are determined. a as example, we will often treat monetary policy systematic response to economic conditions. **Realism Theory and 6.2 1.** simplifying making Macroeconomics proceeds by our in believe literally never We assumptions. in order to see them we need but assumptions, is economy. This an of vast complexity the through endogenous and exog- between distinction the why enous variables is artificial. Truly exogenous vari- but ables are rare. Earthquakes are truly exogenous scientific discov- or about climatic conditions what systematically of inventions? The task and eries endogenous variables to of behaviour the linking accomplished by is exogenous variables in changes variables the all between specifying relationships in economics-and that say might You interest. of of business the in macroeconomics-is particular establishing relationships involving causality. brought together, when these relationships, All social in constitute a theory. Almost by definition, inten- an abstraction, an be must sciences, theory real world the If realism. tional departure from simplifying assump- without could be understood tions, theories would be unnecessary. The problem world's the with rather but economics, with not is friend no was who complexity. Karl Marx, inherent conventional political economy, seemed to hit it of head: the on cells the are than easier to study is The body in its entirety economic forms, moreover, of analysis the In y. bod that of e.us of chemical reagents are nor microscopes herneit 7} ((186 both. replace must abstraction of force The _Kapital) as D_ I, Foreword to Volume 22 **PART** I INTRODUCTION TO MACROECO NOMICS Progress is made by weeding out those assump- tions and theories that lead us to false conclusions. As time passes, some theories prove to be unfounded, while others gain acceptability. This process is long and complex, and far from com- plete. Because macroeconomics is a young disci- pline, a number of controversies continue, and this aspect is discussed in Section 1.7. **1.6.3 Positive and Normative Analysis** Macroeconomic analysis and policy are closely linked. Because a number of exogenous variables are under the control of government, it makes sense to ask what is good and what is bad policy. At its best, macroeconomics can explain the economy. For example, it can link particular events to exoge- nous events or policy decisions. This is **positive eco- nomics:** it refrains from value judgements. **Normative economics** takes a further step and passes judge- ment or makes policy recommendations. In so doing, it must specify what criteria are used in arriving at particular conclusions. This inevitably implies a value judgement. Economists generally like to make policy recommendations. As long as they are truthful about their own preferences and reveal their criteria, this is part of their profes- sional activity. In this textbook, we will generally refrain from normative economic analysis. 6 At the same time, we believe and hope that many readers will make use of their newly acquired knowledge to indulge in the normative side of macroeconom- ics: this is what makes it fun. **1.6.4 Testing Theories: The Role of Data** The generally accepted way of evaluating theories is to subject them to scientific testing. In macroeco- nomics, this means looking at the facts, i.e. at data. This is easier said than done, and there are a num- ber of unusual difficulties. First, data often corres- pond to elusive concepts, as Chapter 2 will show. Second, constructing aggregate data implies enquiring into the behaviour of millions of indi- viduals, who sometimes have good or bad reasons (^6) Many are motivated by 'social conscience' to study economics. Much like idealistic health professionals who want to cure the sick, economists can also be interested in ways to provide relief to the disadvantaged and suffering. to misrepresent the truth. Third, economics shares a predicament common to other social sciences: experimentation is not really possible-when observed, people often change their behaviour. Not only is it possibly immoral-no macroeconomist would wish to start a hyperinflation just to test a theory-but more crucially, many important vari- ables simply are not observable. This is the case of people's expectations of the future, for example. Macroeconomists are forced to conduct empirical tests with the data that they have. They develop statistical techniques, often sophisticated ones, to deal with observation and measurement errors. They refine their techniques for gathering and ana- lysing data. This allows the elimination of inade- quate theories and the modification of others. The surviving theories will be those that withstand the test of time in this sc ientific process. **1.6.5 Macroeconomic Modelling and Forecasting** Economists are frequently asked to make forecasts. Governments, international organizations, and large financial institutions employ large teams of econo- mists to prepare them. If macroeconomics were to be judged by the performance of forecasts, the ver- dict would not be unkind. However, the respectable track record of forecasters has been sullied by some large historical errors. Box 1.3 illustrates this fact by examining the accuracy of forecasts, after the fact, for the disastrous crisis years 2009 and 2010. There are several reasons why economic fore- casting is inherently difficult. First, even an exce llent understanding of an economy's struc- ture-how its endogenous variables interact- can fall victim to unexpected changes in exoge- nous variables. Good examples of this are the oil price increases of 1973 and 2000, their fall in 2015-2016, the high-tech crash of 2001 and, of course, the latest crisis. Second, expectations- which are volatile in nature-wield an important influence over the economy. Governments some- times react to their own forecasts by implement- ing policies designed to prevent those forecasts from happening. Political changes occur quickly and can disrupt the economic environment. Finally, it takes time-often several months-to