Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

Information about the University of Wisconsin-Platteville, including its history, academic programs, and financial report highlights for the fiscal year 2019-20. The university offers over 40 academic programs through three colleges, and has a legacy of academic excellence. The financial report highlights include information about the UW System's Total Net Position, research expenditures, and significant changes within Cash and Cash Equivalents and the UW System's share of the State's pension and other post-employment benefit programs.

Typology: Study notes

1 / 102

This page cannot be seen from the preview

Don't miss anything!

Published by the Office of Finance University of Wisconsin System 1220 Linden Drive Madison, WI 53706

Editor: Rod Dole

Cover Photo: University of Wisconsin–Platteville students walk by Ullrich Hall, which was originally built in 1916 and served as the university's gymnasium and auditorium. The oldest building on campus, Ullrich Hall is listed on the National Register of Historic Places. Currently, Ullrich is now home to classrooms used by accounting, business, computer science, and software engineering as well as lab space for computer science and software engineering. The building is named after Fred Ullrich, who joined the faculty of the Platteville Normal School as an instructor in biological sciences in 1914, and later served as director of the agriculture school.

Founded in 1866 as the first teacher preparatory institution in the state of Wisconsin, UW-Platteville has a legacy of academic excellence that has helped thousands of students find their direct path to success. Today, UW-Platteville offers 40+ academic programs designed to help every student succeed professionally and personally. Programs are offered through three colleges: College of Business, Industry, Life Science and Agriculture, College of Engineering, Mathematics and Science, and College of Liberal Arts and Education.

At UW-Platteville, students enjoy the advantages of a large university in a small, supportive, and safe environment featuring challenging academics, opportunities for undergraduate research, state-of- the-art labs and facilities, and renowned faculty.

Photo Credit: UW-Platteville

Tommy G. Thompson, Interim President

Sean P. Nelson, Vice President for Finance

Robert G. Cramer, Vice President for Administration

Scott Neitzel, Interim Vice President for University Relations

Anny Morrobel-Sosa, Vice President for Academic and Student Affairs

Quinn Williams, General Counsel

Julie Gordon, Senior Associate Vice President for Finance

Ginger Hintz, Assistant Vice President for Financial Administration and Controller

Rod Dole, Director of Financial Reporting

Renee Stephenson, Assistant Vice President of Budget Development and Planning

Charles Saunders, Director for Trust Funds/Assistant Trust Officer

James Schmidt, UW-Eau Claire Michael Alexander, UW-Green Bay Joe Gow, UW-La Crosse Rebecca M. Blank, UW-Madison Mark Mone, UW-Milwaukee Andrew J. Leavitt, UW-Oshkosh Deborah Ford, UW-Parkside Dennis J. Shields, UW-Platteville Connie Foster, UW-River Falls, Interim Bernie L. Patterson, UW-Stevens Point Katherine P. Frank, UW-Stout Renée Wachter, UW-Superior Dwight C. Watson, UW-Whitewater

Robert Atwell, Sturgeon Bay Scott Beightol, Wales Amy Bogost, Madison Héctor Colón, New Berlin José Delgado, Brookfield Michael Grebe, Mequon (Regent Vice President) Eve Hall, New Berlin Mike Jones, Milwaukee Tracey Klein, Brookfield Becky Levzow, Rio Edmund Manydeeds III, Eau Claire Andrew S. Petersen, Middleton (Regent President) Cris Peterson, Grantsburg Corey Saffold, Fitchburg Carolyn Standford Taylor, Madison Karen Walsh, Madison Kyle Weatherly, Milwaukee Olivia Woodmansee, New Glarus

the program’s net assets ($67.9 million) as a Noncurrent Asset.

Within the Statement of Revenues, Expenses, and Changes in Net Position:

portion of the funds were needed to address other COVID-related costs as well.

Although all COVID-19 impacts are not yet known and continued uncertainties are likely in the financial investment markets, the UW System has made and will continue to make necessary fiscal adjustments with the objective of maintaining quality instruction, research and public service, while keeping our students and employees safe.

Sean P. Nelson, Vice President for Finance

The following discussion and analysis provides an overview of the financial position and activities of the University of Wisconsin System (University) for the years ended June 30, 2020 and 2019, with comparative information for the year ended June 30, 2018, where appropriate. This discussion has been prepared by management, is unaudited, and should be read in conjunction with the financial statements and footnotes.

The University is made up of 13 four-year universities and 13 additional campuses affiliated with seven of the four-year institutions. In academic year 2019-2020, the University enrolled 167, students, employed approximately 33,015 faculty and staff, and granted 37,893 associate, bachelor’s, master’s, and other advanced degrees. University institutions were awarded over $1,096.3 million in federal grants and contracts in fiscal year 2020 and an additional $639.4 million from non-federal sponsors. The University has a long tradition of public service, embodied by an ongoing commitment to the Wisconsin Idea, that the boundaries of the University are the boundaries of the State.

Degrees Granted Headcount Enrollments UW-Madison 11,230 UW-Madison 44, UW-Milwaukee 6,053 UW-Milwaukee 26, UW-Eau Claire 2,365 UW-Eau Claire 11, UW-Green Bay 1,526 UW-Green Bay 8, UW-La Crosse 2,380 UW-La Crosse 10, UW-Oshkosh 2,776 UW-Oshkosh 15, UW-Parkside 946 UW-Parkside 4, UW-Platteville 1,888 UW-Platteville 8, UW-River Falls 1,346 UW-River Falls 5, UW-Stevens Point 1,918 UW-Stevens Point 8, UW-Stout 1,878 UW-Stout 8, UW-Superior 607 UW-Superior 2, UW-Whitewater 2,980 UW-Whitewater 12, Total 37,893 Total 167,

The University’s annual financial report includes the Statement of Net Position; the Statement of Revenues, Expenses, and Changes in Net Position; the Statement of Cash Flows; and the Notes to the Financial Statements. These items are prepared in accordance with standards established by the Governmental Accounting Standards Board (GASB).

The Statement of Net Position is a financial condition snapshot as of June 30, 2020 and 2019, and includes all assets and deferred outflows of resources, and liabilities and deferred inflows of resources, with the difference between the two reported as net position. Current assets are those that are available to satisfy current liabilities inclusive of assets that will be converted to cash within one year. Current liabilities are those that will be paid within one year. Increases or decreases in net position provide an indicator of the improvement or erosion of the University’s financial health when considered in conjunction with non-financial information, such as conditions of facilities and enrollment levels. Net Position is divided into three major categories: Net Investment in Capital Assets, Restricted, and Unrestricted. Net Investment in Capital Assets consists of capital assets

The University’s total net position remained stable after fiscal year 2020. As of June 30, 2020, the University had total assets of $8.9 billion and total liabilities of $3.1 billion.

Statement of Net Position (in millions) 2020 2019 2018 Current Assets $ 2,432.5 $ 2,298.0 $ 2,312. Capital Assets, Net 5,345.4 5,258.4 5,140. Other Noncurrent Assets 1,092.3 612.8 986. Total Assets 8,870.2 8,169.2 8,439.

Deferred Outflows of Resources 1,183.4 1,340.4 750.

Current Liabilities 702.4 658.6 661. Noncurrent Liabilities 2,429.0 2,654.7 2,248. Total Liabilities 3,131.4 3,313.3 2,910.

Deferred Inflows of Resources 1,522.7 836.6 849.

Net Investment in Capital Assets 3,574.4 3,614.4 3,519. Restricted Net Position 1,748.5 1,197.6 1,600. Unrestricted Net Position 76.6 547.7 310. Total Net Position $ 5,399.5 $ 5,359.7 $ 5,430.

Current assets minus current liabilities represents the net working capital of the University. Net working capital increased from $1,639.4 million at June 30, 2019 to $1,730.1 million at June 30, 2020. The net working capital at year end represented approximately 120 days of 2020 operating expenses. This indicates that the University could support normal operations for 120 days without additional revenues or liquidating noncurrent assets.

The following table contains a summary of Current Assets which consists primarily of operating cash and cash equivalents, securities lending collateral, accounts receivable, student loans receivable, supply inventories, and prepaid expenses. The largest change between 2020 and 2019 was in cash and cash equivalents, which increased by $85.4 million due to the issuance of state bonds in June 2020.

Current Assets (in millions) 2020 2019 2018 Cash & Cash Equivalents $ 1,949.1 $ 1,863.7 $ 1,868. Securities Lending Collateral 109.4 109.3 106. Accounts Receivable, Net 285.8 249.0 259. Other Current Assets 88.2 76.0 78. Total Current Assets $ 2,432.5 $ 2,298.0 $ 2,312.

The Board of Regents has authority to invest gifts and bequests received by the University. Through March 2018, investments were primarily held in two investment pools: The Long Term Fund and the Intermediate Term Fund. Effective April 1, 2018 and as permitted through Section 36.11 (11m) of the Wisconsin statutes, the Board of Regents transferred its investment management responsibilities to the State of Wisconsin Investment Board (SWIB). As a result of this transfer, the Board of Regents eliminated the Intermediate Term Fund as a separate investment pool. The Board of Regents

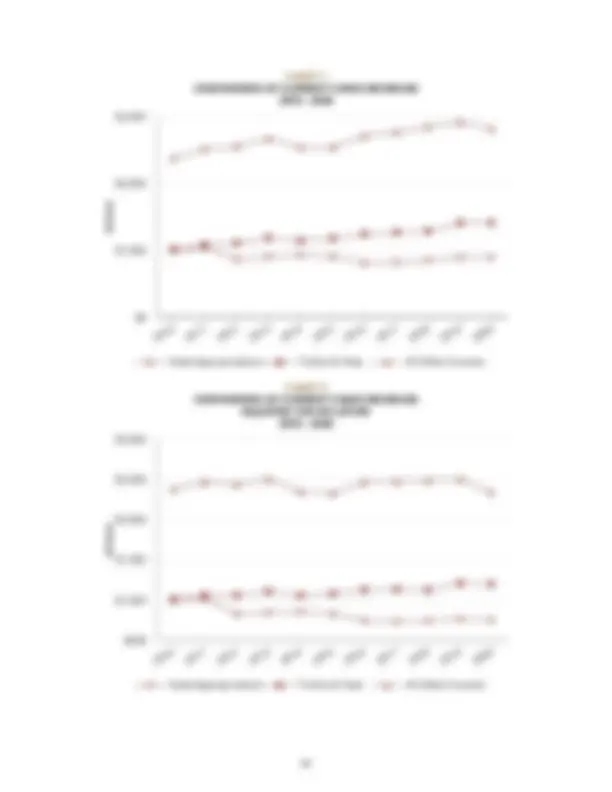

establishes investment policies and guidelines, including target investment allocations. Benefiting UW entities receive quarterly distributions from the Long Term Fund, principally endowed assets, based on an annual spending rate applied to a twelve‑quarter moving average market value of the Fund. A comparison of university-controlled endowments over the past several years can be found in Chart 3 of the Supplemental Information section of this report. Additional information on cash and investments is provided in Note 2 to the Financial Statements.

Non-current assets are comprised mainly of endowment investments, capital assets (net of accumulated depreciation), and student loans receivable. Notable changes between years include:

Deferred outflows decreased by $157.0 million in fiscal year 2020, due to adjustments related to pension and OPEB obligations.

Non-current liabilities decreased by $225.7 million in fiscal year 2020. The most significant reason for this is the adjustment to the pension plan fiduciary net position, as noted above.

Deferred inflows increased by $686.1 million in fiscal year 2020, due to adjustments related to pension and OPEB obligations.

Further, these reporting changes resulted in $34.1 million of additional pension expense being included on the Statement of Revenues, Expenses, and Changes in Net Position. These changes are more fully described in Notes 1 and 8 to the Financial Statements.

Most of the unrestricted net position has been identified for purposes to fulfill the University's fiduciary responsibilities, including academic and research programs and capital projects. Additional information related to net position can be found in Note 13 to the Financial Statements.

Capital and Debt Activities

Of the $5.4 billion in net position, $3.6 billion is net investment in capital assets. In an effort to maintain quality in the University’s academic and research programs and residence halls, the University has implemented a long-range plan to fund new construction and modernize existing facilities. Capital additions consist of new construction, replacement and renovation of academic and research facilities, as well as significant investment in technology and equipment. Note 4 to the Financial Statements describes the University’s capitalization and depreciation policies, and includes summarized changes in the book value of these assets, including major construction projects completed or in progress. Note 6 to the Financial Statements describes the University’s long term debt and includes summarized information on those balances, as well as future debt service requirements.

The University’s operating and non-operating revenues are provided in the table below. Operating revenues decreased $48.2 million since fiscal year 2018 with the primary decrease in sales and services of auxiliaries and all other operating revenues. Non-operating revenues increased $94.2 million between fiscal year 2018 and fiscal year 2020 primarily due to changes in state appropriations, gifts and federal CARES Act funding. The University was awarded $99.3 million in federal funding through the Coronavirus Aid, Relief, and Economic Security (CARES) Act during 2019-20. In accordance with the CARES Act, the University must meet certain eligibility requirements before recognizing the funding. The University recognized $72.3 million as non-operating revenue in 2019-20 and will recognize the remaining amount in 2020-21. These funds are restricted and must be used to address unforeseen financial needs created by the COVID-19 public health emergency, such as personal protective equipment, emergency student grants, housing and dining refunds and technology to accommodate remote learning.

Revenues (in millions): 2020 2019 2018 Operating Revenues Student Tuition and Fees, Net $ 1,407.9 $ 1,402.3 $ 1,382. Federal Grants and Contracts 685.0 617.0 599. State, Local, & Private Grants and Contracts 421.2 447.5 432. Sales and Services of Educational Activities 338.6 371.8 319. Sales and Services of Auxiliaries, Net 354.3 433.6 445. All Other Operating Revenues 461.6 469.0 537. Total Operating Revenues 3,668.6 3,741.2 3,716.

Non-Operating Revenues State Appropriations 885.3^ 883.6^ 838. Gifts 382.3^ 395.7^ 370. Federal Pell Grants 149.6^ 160.0^ 162. Federal CARES Act Grants 72.3^ —^ — Net Investment Income (Loss) 44.0^ 86.4^ 45. Other Non-Operating Revenues 27.7^ 35.1^ 50. Total Non-Operating Revenues 1,561.2 1,560.8 1,466. Total Revenues $ 5,229.8 $ 5,302.0 $ 5,183.

Operating expenses, classified by function, and non-operating expenses, are as follows:

Expenses (in millions): 2020 2019 2018 Operating Expenses Instruction $ 1,314.8 $ 1,452.9 $ 1,257. Research 1,032.0 987.1 984. Public Service 348.7 364.8 298. Academic Support 442.2 428.7 401. Student Services 500.7 505.5 479. Institutional Support 338.7 309.1 311. Operation/Maintenance 312.8 298.9 284. Financial Aid 273.3 243.6 257. Auxiliary Enterprises 298.8 359.7 363. Other Functions 69.3 71.0 81. Depreciation 329.1 327.3 324. Total Operating Expenses 5,260.4 5,348.6 5,044. Non-Operating Expenses 138.5 137.5 124. Total Expenses $ 5,398.9 $ 5,486.1 $ 5,168.

One of the University's strengths has been its ability to supplement student tuition and fee revenue and state appropriations with support from other sources, including foundations, investment income, and government-sponsored programs (see Charts 1 and 2 in the Supplemental Information of this report). The University continues to aggressively seek funding sources consistent with its mission to meet operating activities in a financially prudent manner. In addition, the University will continue to make cost containment and revenue diversification a priority. Increase in Instruction operating expenses during fiscal year 2019 is attributed to the increase in pension plan expense reported within salary and fringe benefits expense, as compared to fiscal year 2020 and 2018.