Download Principles of Microeconomics Exam (Econ 002) - Drake University, Spring 2007 - Prof. Willi and more Exams Microeconomics in PDF only on Docsity!

Principles of Microeconomics (Econ 002) Signature:

Drake University, Spring 2007

William M. Boal Printed name:

FINAL EXAMINATION VERSION B

May 9, 2007

INSTRUCTIONS: This exam is closed-book, closed-notes. Simple calculators are permitted, but graphing calculators or

calculators with alphabetical keyboards are NOT permitted. Numerical answers, if rounded, must be correct to at least 3

significant digits, but fractions are always acceptable answers. Point values for each question are noted in brackets.

Maximum total points are 200.

SECTION: In which section are you enrolled? Please check one.

CRN 105 meeting at 9:30 in Aliber 10. CRN 107 meeting at 11:00 in Aliber 101.

I. MULTIPLE CHOICE: Circle the one best answer to each question. [2 pt each, 42 pts total]

(1) Is the production function below characterized by

diminishing returns to labor input?

a. Yes, for all levels of labor input.

b. No, not for any levels of labor input.

c. Yes, but only after 100 hours of labor.

d. Yes, but only before 100 hours of labor.

(2) Suppose a student can read 5 pages of mathematics

per hour or 50 pages of history per hour. The student’s

opportunity cost of reading a page of mathematics is

a. 1/50 page of history.

b. 1 page of history.

c. 5 pages of history.

d. 10 pages of history.

e. 45 pages of history.

(3) Orange juice and grapefruit juice are substitutes. If

the price of orange juice rises,

a. the demand curve for grapefruit juice shifts left.

b. the demand curve for grapefruit juice shifts right.

c. the supply curve for grapefruit juice shifts left.

d. the supply curve for grapefruit juice shifts right.

e. none of the above.

(4) In summer, the price of watermelons falls and the

quantity purchased rises. This could be caused by a

a. rightward shift in the supply curve.

b. leftward shift in the supply curve.

c. rightward shift in the demand curve.

d. leftward shift in the demand curve.

(5) In the graph below, which supply curve below is

more elastic?

a. Supply curve A.

b. Supply curve B.

c. Both supply curves are equally elastic because they

pass through the same point.

d. Cannot be determined from information given.

100 Hours of labor

Concrete poured

Q

P

A

B

Drake University, Spring 2007

Page 2 of 14

(6) You have a startup software company. You have

tentatively proposed a price of $50 for your product and

have called on two marketing consultants for advice.

Consultant X says demand for your product is probably

elastic at this price. Consultant Y disagrees and say

demand for your product is probably inelastic at this

price. After reading their reports, you conclude that:

a. to increase sales revenues you should decrease

price if you believe Consultant X, but increase

price if you believe Consultant Y.

b. to increase sales revenues you should hold price

constant since the opposing views of the

consultants suggest demand is unitarily elastic.

c. to increase sales revenues you should increase price

if you believe both consultants.

d. to increase sales revenues you should decrease

price if you believe both consultants.

e. to increase sales revenues you should increase price

if you believe Consultant X, but decrease price if

you believe Consultant Y.

(7) Suppose that as the price of gasoline rises from

$2.50 to $3.50 per gallon, the average customer reduces

monthly gasoline purchases from 30 gallons to 20

gallons. Using the arc or midpoint formula, the

elasticity of demand for gasoline is computed to be

a. – 0..

b. – 0..

c. – 1..

d. – 1..

e. – 1..

f. – 10..

g. none of the above.

(8) Arbitrageurs’ motivation for buying and selling is to

a. make money.

b. enforce the Law of One Price.

c. keep markets orderly.

d. ensure that all consumers face a fair price.

e. all of the above.

(9) Speculation through buying and holding inventories

will tend to

a. raise the price of a good today and lower it in the

future.

b. ensure adequate supply for future consumption.

c. encourage conservation today.

d. all of the above.

e. none of the above.

(10) Who benefits from a price floor or legal minimum

price?

a. All sellers.

b. All buyers.

c. Some sellers.

d. Some buyers.

e. All buyers and all sellers.

f. No one.

(11) Suppose the price elasticity of demand for sodapop

is -0.4 and the price elasticity of supply of sodapop is

6.0. If a tax is imposed on sodapop, which side of the

market effectively pays most of the tax?

a. Sellers pay most of the tax.

b. Buyers pay most of the tax.

c. Sellers and buyers each pay half of the tax.

d. Answer depends on which side is legally required

to remit the tax to the government.

(12) Ryan’s indifference-curve diagram is shown below.

The straight line represents Ryan’s budget line and the

curved lines represent his indifference curves. If Ryan

is currently choosing the bundle of goods represented by

point A, Ryan could be made better off without

exceeding his budget by

a. buying more food and fewer other goods.

b. buying more other goods and less food.

c. either (a) or (b).

d. Ryan cannot be made better off by changing his

purchases.

(13) If a firm is currently producing at a level of output

where marginal cost is less than marginal revenue, it

can increase its profit by

a. producing less output.

b. producing more output.

c. It cannot increase its profit by making small

changes in output.

d. Cannot be determined from information given.

Food

Other goods

A

Drake University, Spring 2007

Page 4 of 14

(18) Consider the behavior of a monopolist who does

not engage in price discrimination. Which of the

following is TRUE?

a. Because of its monopoly power, the monopolist is

able to produce at the lowest point of its average

cost curve, allowing the firm to earn more

economic profit than a competitive firm.

b. Since the monopolist is able to earn an economic

profit in both the short and long run, it is efficiently

allocating resources to the production of goods and

services demanded by consumers.

c. By maximizing its economic profit, the monopolist

maximizes total consumer and producer surplus,

even if it keeps most of that surplus for itself.

d. The monopolist will never choose to operate in the

elastic portion of the demand curve.

e. None of the above is true.

(19) Other things being equal, if a perfectly competitive

industry evolves into a cartel, the output of the industry

will likely __________ and the price of the output will

likely __________.

a. remain unchanged; increase

b. increase; increase.

c. decrease; decrease.

d. increase; decrease

e. None of the above.

(20) If the market in the graph below is competitive, the

equilibrium quantity will be

a. 20 thousand , the quantity that maximizes output

and consumer surplus.

b. 8 thousand, the quantity that maximizes sellers'

producer surplus.

c. 10 thousand, the quantity that maximizes sellers'

revenue.

d. 14 thousand, the quantity that maximizes consumer

surplus plus producer surplus.

e. none of the above.

(21) Because art museums are buildings (unlike, say,

city parks), it is easy to charge admission. Therefore an

art museum is

a. a rival good.

b. a nonrival good.

c. an excludable good.

d. a nonexcludable good.

e. a normal good.

f. an inferior good.

Quantity (thousands)

Price

Demand

Supply

Drake University, Spring 2007

Page 5 of 14

II. PROBLEMS: Insert your answer to each question in the box provided. Feel free to use the margins for scratch

workonly the answers in the boxes will be graded. Work carefullypartial credit is not normally given for questions in

this section.

Drake University, Spring 2007

Page 7 of 14

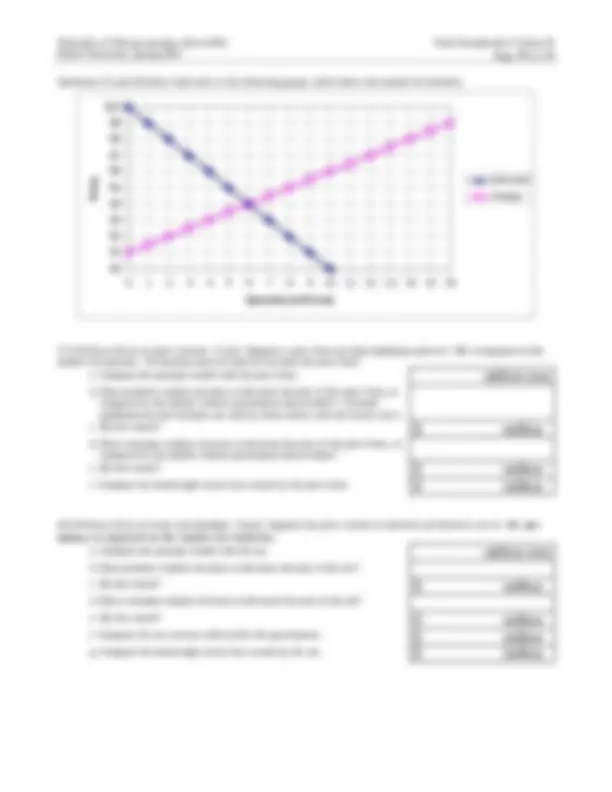

(2) [Market equilibrium: 12 pts] Suppose five buyers

and five sellers engage in a market similar to the

activity we did in class. Each buyer may buy at most

one unit and each seller may sell at most one unit, but

no one is forced to trade. Assume that buyers and

sellers are each trying to maximize their personal

earnings (or “gains from trade”). Earnings for each

buyer equal the buyer's value of the good minus the

price paid. Earnings for each seller equal the price

received minus the seller's cost of the good. Earnings of

persons who do not trade are zero. Prices must be

whole dollars. Buyers’ values and sellers’ costs are

given in the following table.

Buyer Value Seller Cost

Bob $12 Stephani

e

Briana $10 Steve $ 1

Bill $ 3 Sally $ 5

Betty $ 2 Sean $ 5

Bart $ 1 Susan $ 6

Use the graph below for scratch work.

$

$

$

$

$

$

$

$

$

$

$

$

$

$

0 1 2 3 4 5 6

Quantity

Price

a. Suppose the price were $8. Would there be excess demand or excess supply?

b. What is the equilibrium price likely to be, in whole dollars?

c. How many units of the good will be sold in this market?

units

d. Compute the total revenue received by sellers (which equals total spending by

buyers).

e. Who enjoys higher earnings (or gains from trade) in this particular market, the

buyers or the sellers? Or are buyers’ total earnings equal to sellers’ total

earnings?

f. Compute the combined total earnings (or gains from trade) of all buyers and

sellers. (Check your answer carefully!)

(3) [Using price elasticities: 8 pts] Suppose the electric utility company lowers its rates (that is, the price of electricity)

by 5% and the elasticity of demand for electricity is -0.8. Assume nothing else changes.

a. Will the quantity of electricity demanded increase or decrease?

b. ... by approximately how much?

c. Will the total revenue received by the electric utility company increase or

decrease?

d. ... by approximately how much?

Drake University, Spring 2007

Page 8 of 14

(4) [Government farm policies: 10 pts] The following table shows the market for grain.

Price per ton Quantity demanded Quantity supplied

$1 11 million tons 0 million tons

$2 9 million tons 1 million tons

$3 7 million tons 3 million tons

$4 5 million tons 5 million tons

$5 3 million tons 7 million tons

$6 1 million tons 9 million tons

$7 0 million tons 11 million tons

First consider the market without government intervention.

a. Find the equilibrium quantity.

million tons

b. Find the equilibrium price. $ per ton

Now suppose the government sets a target price of $6 per ton.

c. How many tons of grain must the government purchase to raise the price to this

level?

million tons

d. What will be the direct cost of this program to the government--that is, how much

money should the government budget for grain purchases?

$ million

e. How much grain will the private sector purchase at the target price?

million tons

(5) [Effects of international trade: 18 pts] Country #1 and Country #2 both have markets for

soybeans. Supply and demand schedules for the two countries are given below in millions of tons.

Country #1 Country #

Price Quantity demanded Quantity supplied Quantity demanded Quantity supplied

First consider the outcomes under autarky (that is, no international trade).

a. Compute the equilibrium price in Country #1.

$

b. Compute the equilibrium price in Country #2.

$

Now consider the outcomes with free international trade between Country #1 and Country #2.

c. Compute the equilibrium price with trade.

$

d. Which country exports soybeans?

e. How much soybeans does that country export? million tons

Indicate whether each of the following groups are better off, worse off, or just as well off as before , as a result of free

international trade.

f. Soybean consumers in

Country #1.

h. Soybean consumers

in Country #2.

g. Soybean producers in

Country #1.

i. Soybean producers in

Country #2.

Drake University, Spring 2007

Page 10 of 14

Questions (7) and (8) below both refer to the following graph, which shows the market for batteries.

Quantity (millions)

Price

Demand

Supply

(7) [Welfare effects of price controls: 12 pts] Suppose a price floor (or legal minimum price) of $ 6 is imposed on the

market for batteries. No batteries may be sold for less than the price floor.

a. Compute the quantity traded with the price floor. million tons

b. Does producer surplus increase or decrease because of the price floor, as

compared to the market without government intervention? (Assume

optimistically that batteries are sold by those sellers with the lowest cost.)

c. By how much?

$ million

d. Does consumer surplus increase or decrease because of the price floor, as

compared to the market without government intervention?

e. By how much? $ million

f. Compute the deadweight social loss caused by the price floor.

$ million

(8) [Welfare effects of taxes and subsidies: 14 pts] Suppose the price control is removed and instead a tax of $ 6 per

battery is imposed on the market for batteries.

a. Compute the quantity traded with the tax. million tons

b. Does producer surplus increase or decrease because of the tax?

c. By how much?

$ million

d. Does consumer surplus increase or decrease because of the tax?

e. By how much?

$ million

f. Compute the tax revenue collected by the government.

$ million

g. Compute the deadweight social loss caused by the tax. $ million

Drake University, Spring 2007

Page 11 of 14

(9) [Monopoly: 12 pts] Suppose Acme Game Company has a monopoly in the market for a particular copyrighted video

game. Its demand, marginal revenue, and marginal cost curves are shown below. Assume for simplicity that marginal

cost equals average cost.

Quantity (thousands)

Demand

Marginal revenue

Marginal cost and

average cost

Assume Acme must charge the same price to all its customers.

a. Suppose Acme were (for some reason) producing 3000 copies of the game. If

Acme produced one more copy, by how much would its total cost increase? That

is, what would be the change in total cost as Acme increased output from 3000 to

3001 copies? (Give an answer to the nearest whole dollar.)

$

b. Again suppose Acme were (for some reason) producing 3000 game sets. If Acme

produced one more copy, by how much would its total revenue increase? That is,

what would be the change in total revenue as Acme increased output from 3000 to

3001 copies? (Give an answer to the nearest whole dollar.)

$

c. What quantity should Acme produce to maximize profits? thousand

d. What price should it charge?

$

e. Compute Acme's profit. $ thousand

f. Compute the deadweight loss from monopoly.

$ thousand

Drake University, Spring 2007

Page 13 of 14

(11) [Externalities: 12 pts] The graph below shows the market for a particular vaccine. A vaccination protects the

purchaser of the vaccine, but also reduces the chances of other people catching the illness. Therefore, in addition to

demand and supply curves, a curve representing marginal social benefit is shown.

Quantity (millions of vaccinations)

Price per vaccination

Demand =

marginal

private

benefit

Supply

Marginal

social

benefit

a. Compute the (unregulated) competitive equilibrium price.

$

b. Compute the (unregulated) competitive equilibrium quantity. million

c. Compute the economically efficient (or socially optimal) quantity. million

d. Compute the deadweight loss from unregulated competition.

$ million

e. To eliminate this deadweight loss, should the government impose a tax or

a subsidy?

f. What should be the tax rate or subsidy rate?

$ per vaccination

Drake University, Spring 2007

Page 14 of 14

III. CRITICAL THINKING: Write a one-paragraph essay answering one question below (your choice). [5 pts]

(1) Consider the following statement: “Free trade is fine in industries where international prices are higher than our

prices, because then American firms and workers can compete. But in industries where international prices are lower

than American prices, we need to restrict international trade to protect our businesses and workers from an international

race to the bottom. American trade policy must benefit Americans.” Do you agree or disagree? Justify your answer

with a graph.

(2) Consider the following statement. "Cartels replace cutthroat competition with stable prices that everyone can

live with. But they need government support—otherwise the law of the jungle takes over and companies undercut each

other. Congress should repeal laws against cartels so businesses can cooperate for the benefit of everyone." Do you

agree or disagree? Justify your answer with a graph.

Please circle the question you are answering. Write your answer below. Full credit requires correct economic reasoning,

legible writing, good grammar including complete sentences, and accurate spelling.

[end of exam]