Financial Analysis Report

Name

Institution

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

This assignment gives you the opportunity to evaluate and critically analyse the selected positions within a company’s annual report. These positions are of crucial importance for obtaining final performance and economic benefits.

Typology: Study Guides, Projects, Research

1 / 20

This page cannot be seen from the preview

Don't miss anything!

Name Institution

Inventories figures are valued in BMW through cost and net realizable value using the weighted average cost method. Adidas uses the first-in, first-out approach (FIFO). Selection of an inventory valuation method can lead to different carrying values and costs of sales for inventories due to changes in the purchase and selling prices. Additionally, BMW and Adidas apply the straight-line method for property, plant, and equipment. However, disparities arise in the estimated useful lives, ranging from 3 to 50 years for BMW and 3 to 40 years for Adidas (Adidas, 2021). Additionally, BMW tests its property, plant, and equipment for impairment whenever there is an indication of impairment, or at least annually, for goodwill and intangible assets with indefinite useful lives. Adidas tests its property, plant, and equipment for impairment whenever there is an indication of impairment, or at least annually, for goodwill and intangible assets with indefinite useful lives. This difference can result in different depreciation and impairment expenses and carrying amounts of property, plant, and equipment, depending on the estimation of useful lives and impairment indicators. In lease accounting, both companies adopt IFRS 16 Leases, recognizing right-of-use assets and lease liabilities, excluding short-term leases and leases of low-value assets. However, differences in defining short-term leases and low-value assets may affect the scope and amount of lease recognition, leading to disparities in financial reporting. Provisions and contingencies handling also diverges. BMW recognizes provisions for warranties, product recalls, and other obligations when a present legal or constructive obligation exists, coupled with a probability of outflow and a reliable estimate. Adidas follows a similar approach but includes provisions for returns. However, BMW and Adidas have different judgments and assumptions in estimating the probability, timing, and amount of the provisions and contingencies, which may affect the completeness and accuracy of the provisions and contingencies.

BMW’s revenue recognition procedure involves following the International Financial Reporting Standards (IFRS). Most of the company’s revenues are generated from its automotive segment, which comprises vehicle sales, spare parts and accessories. For its vehicles, BMW adopts the point-of-delivery approach, whereby it records revenue when there is transfer of control to the customer at delivery. This approach guarantees that revenue is recognized when the customer gets hold of the vehicle directing to the time BMW meets its performance obligation. In addition to the point-of-delivery technique, BMW recognizes revenue from spare parts and accessories throughout time, as the client receives and utilizes the advantages of these items. BMW tailors its revenue recognition process to the particular features of each product category within its automotive segment, using a combination of point-of-delivery and overtime approaches. On the other hand, because of the nature of its business, which encompasses not only the sale of items but also licensing and franchising agreements, the well-known sportswear manufacturer Adidas uses a varied revenue recognition approach. For its clothing, shoes, and hardware products, the business uses the point-of-sale approach, realizing income at the time a consumer makes a purchase. This simple method guarantees that revenue is recorded at the time of client take- possession and is consistent with the physical character of these items. In case of licensing or franchising agreements, Adidas recognizes revenue through delivery on progressive cycles as they fulfil their performance obligations. This involves granting a license or franchise of the freedom to practice the intellectual property and trademarks of Adidas. Considering the consistent benefits derived by the licensee or franchisee from establishing association with Adidas brand, revenue is systematically recognized as per contract period. This overtime method of licensing and franchising agreements recognizes the ongoing value offered to business partners. BMW and Adidas are dedicated to transparency and accuracy in their financial reporting that requires them to select revenue recognition methods based on the nature of products or services. The point-of-delivery and overtime approaches the company uses in its automotive segment highlights BMW’s unique comprehension of transactions based on revenue generating moments. In the same way, Adidas' decision to use the point-of sale approach for

to purchase shares at a certain price within a predetermined time frame (Adidas, 2021). Similar to BMW, Adidas sees these equity compensation programs as a means of involving staff members in the overall success and future prospects of the business. The executive remuneration of BMW consists of a fixed salary, annual performance bonus, long- term incentive plan, and pension package. A monthly fixed salary is paid based on an individual’s responsibilities. The long-term incentive plan has four years of performance period, giving cash awards that are equal to the number of BMW shares based on relative total shareholder return and earnings per share. Pension benefits are defined contribution, which contributes to the pension fund according to age and salary. Adidas adopts a five-component executive compensation system, including fixed salary, annual performance bonus, long-term incentive plan, pension allowance, and benefits. Similar to BMW, the fixed salary depends on responsibilities and experience. The annual bonus aligns with financial and non-financial targets. Adidas' long-term incentive plan spans five years, offering a cash payment equivalent to Adidas shares based on relative total shareholder return and environmental, social, and governance targets. The pension allowance replaces the previously defined contribution plan, and benefits encompass various non-cash perks. Stock compensation schemes by both BMW and Adidas grant employees’ stock options, restricted stock units, and share save plans. BMW has a vesting period of four years and an exercise window of ten years for stock options offered to its senior managers. With a three-years vesting period, restricted stock units to senior executives are handled by Adidas in either cash or share settlement. Offering employee share purchase plans, both companies enable eligible employees to buy shares at a lower price, subject to waiting period. The success of stock compensation plans stems from the fact that they help to create a connection between employee and shareholder incentives. Since employees own part of a company, they tend to make decisions and engage in actions that support its lasting success. This is consistent with the shared value creation concept whereby there are benefits to both the organization and its members by way of prolonged expansion and earnings. However, openness and information sharing about the stock compensation plans are critical aspects of their efficacy. BMW and Adidas have to make sure that the employees understand these plans clearly as proper communication of the issues

regarding them will be a need. This communication builds and supports trust and commitment among employees while increasing the connection between individual performance, firm results. Moreover, the transparencies and communications relating to stock compensation plans are paramount for their viability. Both BMW and Adidas must efficiently inform employees about the details of these plans to leave no doubts regarding the advantages and obligations. This form of communication contributes to the development of trust and employee engagement, strengthening the connection between individual performance and business performance.

Statement of Cash Flows is an important financial statement that provides details about cash flows from the operation, investment, and financing activities. BMW and Adidas demonstrate distinct investment strategies and focuses using their cash flows that invest. The negative trend of BMW’s investing cash flows has been steadily increasing for the past three years, which suggests that there have been significant outflows of cash in purchasing fixed long term assets such as property, plant, and equipment or innovative investments. The reason is due to BWM’s strategic emphasis on increasing production capacity, improving technological competence and creating product-service variety, especially fields such as electrification, digitalization and sustainability. On the other hand, Adidas also provides information on the negative investing cash flows but with variations. The company's investing activities, while still involving significant cash outflows, are more moderate compared to BMW. However, Adidas focuses on enhancing operational effectiveness as well as brand equity and market share growth, especially in emerging markets and online channels. Adidas AG Cash Flow from Financial Activities Adidas AG has faced a significant downward trend in the cash flow from financial activities as it reported a 59.48% and 65.06% year-over-year decrease for quarter and twelve months ending September 30,2023 respectively The annual trend is also a sharper decrease, with an outstanding 746.73% reduction in 2021 as compared to the previous year (Macrotrends, 2022). This implies that there was a significant decline in cash used for funding activities suggesting problems securing external funds or debt management. While the negative cash flow in recent years

capital management. On the other hand, Adidas has positive and fluctuating cash flows from financing activities for the same period implying that more funds have been raised by lenders than repaid. Adidas funds its operations through external debt and equity, using money from the issuance of borrowings and sales of treasury shares to offset dividends paid by shareholders as well as repayment of borrowings and purchases of treasury stocks (Macrotrends, 2022). This reflects the fact that Adidas has a high leverage, flexible capital structure, and opportunistic capital allocation. The analysis of investing and financing cash flows allows us to draw several conclusions about BMW and Adidas: High and stable cash outflows of BMW indicate firm commitment to the long-term growth path through significant investments into production capacity, technology, and diversification. On the other hand, Adidas takes a more moderate investment stance by targeting operational efficiency, brand strength and market share growth. Further, BMW tends to focus on internal cash generation and emphasizes shareholder returns, indicating the company’s constant negative financing cash flows. On the contrary, Adidas relies mainly on external financing using both debt and equity. This demonstrates the capability of Adidas to be flexible with its capital structure and search for external funding opportunities. Furthermore, BMW has greater and more consistent operational cash flows but displays more unstable investing and financing cash flows. This implies that though BMW’s main activities are sources of stable cash, the investments and financing activities contribute to variations. The fact that Adidas’s operating cash flows are lower and more volatile is compensated by higher, relatively less variable investing and financing cash flows, probably helping to reduce overall cash flow risk.

The strategic developments and growth of BMW AG are made possible through its investments in subsidiaries and participations. According to the financial statements for the year 2020 reveal considerable investment in subsidiaries and participations amounting to €12,093 million representing an increase of 13.8% over the previous year (Adidas Annual Report 2022, 2022). This shows that BMW invests strategically in order to fulfil its long-term objectives Second, this development reflects a strategy to scale up the firm’s business portfolio. Among the highlighted

investments is BMW’s takeover of a majority stake in BMW Brilliance Automotive (BBA) done in 2020. This investment, involving a total of €3.6 billion not only manifests the major financial commitment but also demonstrates BMW’s keen interest in the Chinese market (BMW Annual Report, 2022). The decision to increase its shareholding from 50% to 75% in BBA aligns with BMW's aim to strengthen its position in China, the largest and fastest-growing market for the company. The improved result on investments, growing from €1,858 million in 2019 to €3,084 million in 2020, indicates that BMW's strategic investments are yielding positive returns. The financial statements specify that investments in subsidiaries and participations are stated at cost or fair value, reflecting a prudent approach to valuation. Moreover, BMW's diversification into electric mobility and digitalization is evident through investments in subsidiaries like BMW i Ventures, BMW Startup Garage, and BMW Digital Ventures (BMW Annual Report 2022, 2022). These entities focus on fostering innovation and solutions in mobility, sustainability, and customer experience, showcasing BMW's commitment to staying at the forefront of technological advancements. Investing in research and development is another aspect where BMW directs significant funds. In 2020, the company allocated €5,394 million to research and development expenses, emphasizing its dedication to innovation and staying competitive in the rapidly evolving automotive industry. Adidas, as stated in its Annual Report 2022, is also involved in strategic investments subsidiaries, associates and joint ventures. As of December 31, 2022, the total carrying amount of investments in subsidiaries was €3,163 million representing a significant increase of €1,021 million compared to last years value(Adidas Annual Report 2022, 2022). The growth is mainly attributed to the acquisition of Allbirds, Inc. as a reflection of how far Adidas will go in building its portfolio. Moreover, Adidas makes investments in associates and joint ventures by digitalization, sustainability, and innovation aspects. The carrying amount for these investments increased by €366 million, marking the company's intention to align with emerging trends and technologies. In particular, the result was bolstered by fair value gains from investments in businesses such as Carbon Inc. and Peloton Interactive Inc. The diversification into sustainability is evident through investments in Worn Again Technologies Ltd., a developer

Significance of Goodwill Values The growing positive in goodwill reflects BMW’s intent to acquire entities that have high impact on its brand, customer base and innovative services. The significant positive value associated with goodwill leaves BMW well poised to grow and thrive in the future as a competitive firm. The opposite situation is true of the negative trend in Adidas’s goodwill and impairments, which point to obstacles for merging and retrieving value from its acquisitions. The structural change, involving the sale of Reebok among others is a signal that further analysis and possibly restructuring would be adequate for negotiations with market forces so as to reduce risk. Strategic Implications Stable and increasing goodwill of BMW suggest considered approach to acquisitions, which are consistent with the company objective. The fact that impairment did not occur in 2022 highlights the successful oversight of risks and due diligence with respect to cash generating units’ recoverable amount for 2015, 2016, and 2017. On the other hand, impediments to and impairments of Adidas’s goodwill imply that strategic adjustment is necessary including selling their companies and more cautious attitude towards future acquisitions. In turn, the influence of COVID-19 reinforces the notion that flexibility and resistance to external factors are crucial.

In conclusion, a thorough financial analysis of BMW and Adidas reveals the complexities of these two giants in the global business. Although the two companies follow a same accounting framework, their policies of accounting, methods of revenue recognition and compensation structures show variations that reflect their respective approaches to strategies and industry challenges. BMW's initiatives to sustained expansion has been evaluated by emphasizing on its strategic investments, especially in its subsidiary ventures. On the other hand, Adidas has more efficient investment approach, which prioritise operational efficiency and expanding its market share. The assessment of cash flows as well as investments in subsidiaries are also considered as their distinct strategies. This analysis provides valuable insights to stakeholders, which allows

them to comprehend the financial landscape in order to make informed choices in a dynamic global commercial market.

Adidas. (2021). Board compensation. adidas Annual Report 2021. https://report.adidas- group.com/2021/en/to-our-shareholders/compensation-report/board-compensation.html Adidas. (2022). Financial instruments. adidas Annual Report 2022. https://report.adidas- group.com/2022/en/consolidated-financial-statements/notes/notes-to-the-consolidated-statement- of-financial-position/financial-instruments.html BMW-AG. (2022). BMW-AG-Financial-Statements-2022. https://www.bmwgroup.com/en/report/2022/downloads/BMW-AG-Financial-Statements-2022- en Herzogenaurach,. (2023). Adidas results in 2022 reflect geopolitical, macroeconomic, and company-specific challenges. https://www.adidas-group.com/media/filer_public/b7/a3/b7a3a513-50a9-41ca-b48b- ace4b889527e/20230308_adidas_ag_fy2022_results_en Macrotrends Bmw. (2023). BMW Goodwill and Intangible Assets 2010-2023 | BAMXF. https://www.macrotrends.net/stocks/charts/BAMXF/bmw/goodwill-intangible-assets-total Macrotrends. (2022). BMW Cash Flow from Investing Activities 2010-2023 | BAMXF. macrotrends. https://www.macrotrends.net/stocks/charts/BAMXF/bmw/cash-flow-from- investing- Macrotrends. (2022). BMW Goodwill and Intangible Assets 2010-2023 | BAMXF. https://www.macrotrends.net/stocks/charts/BAMXF/bmw/goodwill-intangible-assets-total Macrotrends. (2023). Adidas AG Goodwill and Intangible Assets 2010-2023 | ADDYY. https://www.macrotrends.net/stocks/charts/ADDYY/adidas-ag/goodwill-intangible- assets-total Stockanalysis. (2023). Adidas ag (Etr: Ads) cash flow statement. Stock Analysis. https://stockanalysis.com/quote/etr/ADS/financials/cash-flow-statement/

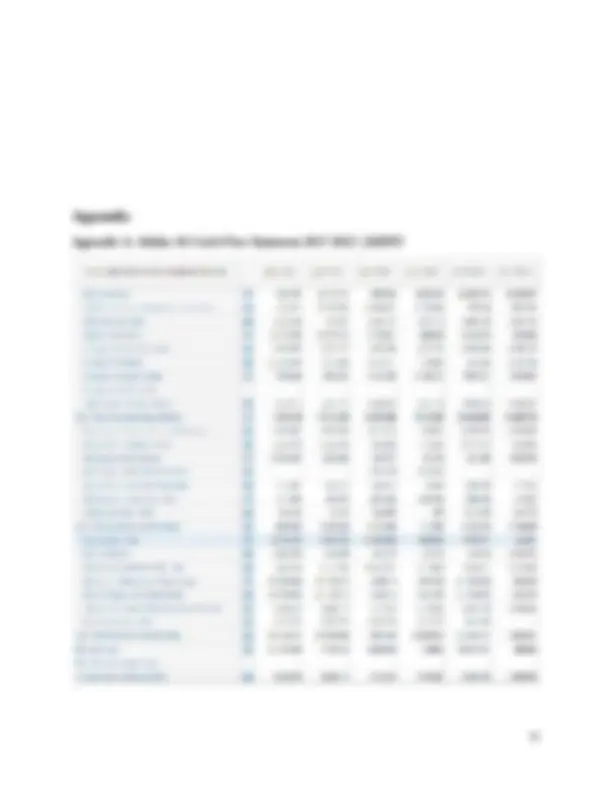

Appendix B: BMW Cash Flow Statement 2018-2022 | BAMXF

Appendix E: BMW Cash Flow from Investing Activities 2010-2023 | BAMXF Appendix F: Adidas AG Cash Flow from Investing Activities 2010-2023 | ADDYY

Appendix G: BMW Cash Flow from Financial Activities 2010-2023 | BAMXF Appendix H: Adidas AG Cash Flow from Financial Activities 2010-2023 | ADDYY