150 West Main Street, Suite 1700 | Norfolk, Virginia 23510

www.wstam.com | 757.623.3676

Economic and Market Overview

December 2021

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

An economic and market overview for December 2021, discussing the global growth stall caused by COVID-19, labor issues, and supply chain disruptions. Inflation is also addressed, with the Fed's stance on its transitory nature being questioned. equity and bond market performance, including U.S. large cap growth, value, small-cap, and international stocks. It also discusses the yield curve and the importance of credit exposure.

What you will learn

Typology: Lecture notes

1 / 18

This page cannot be seen from the preview

Don't miss anything!

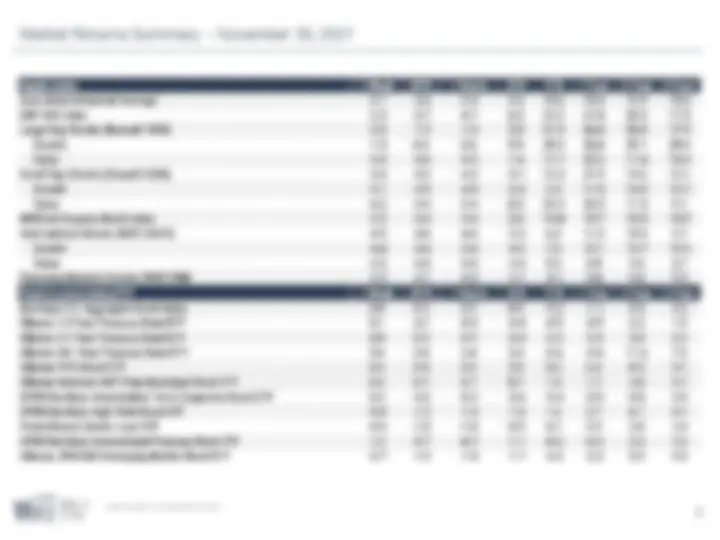

Executive Overview Some of the information enclosed may represent opinions of WST which are subject to change from time to time and which do not constitute a recommendation to purchase and sale any security nor to engage in any particular investment strategy. There are no guarantees investment objectives will be met. Worries Mount As Year End Approaches

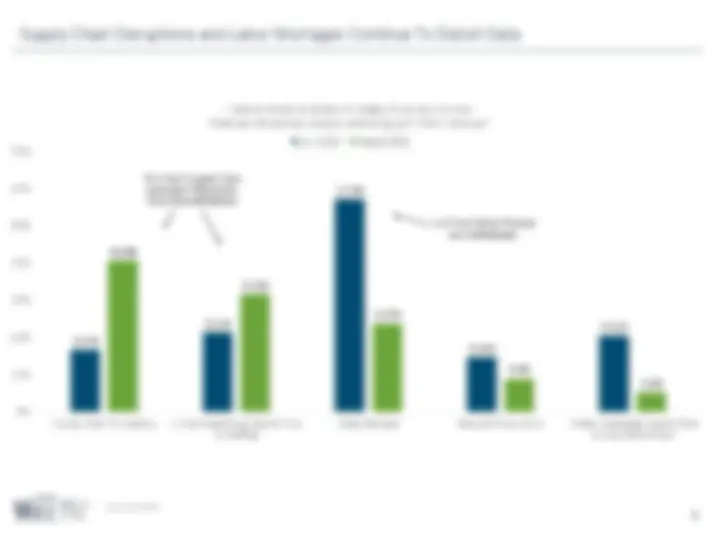

Supply Chain Disruptions and Labor Shortages Continue To Distort Data Source: Glenmeade.

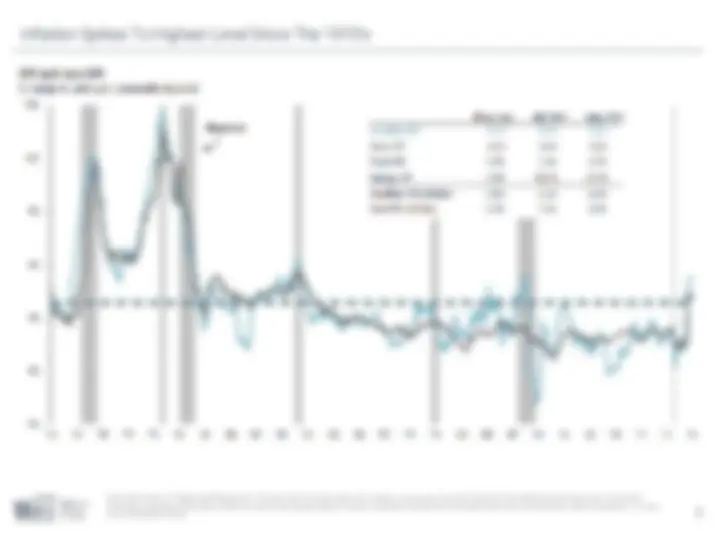

5 Inflation Spikes To Highest Level Since The 1970’s Source: BLS, FactSet, J.P. Morgan Asset Management. CPI used is CPI-U and values shown are % change vs. one year ago. Core CPI is defined as CPI excluding food and energy prices. The Personal Consumption Expenditure (PCE) deflator employs an evolving chain-weighted basket of consumer expenditures instead of the fixed-weight basket used in CPI calculations. Guide to the Markets – U.S. Data are as of September 30, 2021.

7 S&P 500 – Rally Stalls In September Source: Compustat, FactSet, Federal Reserve, Standard & Poor’s, J.P. Morgan Asset Management. Dividend yield is calculated as consensus estimates of dividends for the next 12 months, divided by most recent price, as provided by Compustat. Forward price-to-earnings ratio is a bottom-up calculation based on J.P. Morgan Asset Management estimates. Returns are cumulative and based on S&P 500 Index price movement only, and do not include the reinvestment of dividends. Past performance is not indicative of future returns. Guide to the Markets – U.S. Data are as of September 30, 2021.

U.S. Equity Valuations and Subsequent Returns Source: Robert Shiller, Bloomberg and Goldman Sachs Asset Management.

10 Size: Disparity Between Mega-Cap and All Others Source: FactSet, Standard & Poor’s, J.P. Morgan Asset Management. The top 10 S&P 500 companies are based on the 10 largest index constituents at the beginning of each month. The weight of each of these companies is revised monthly. As of 9/30/21, the top 10 companies in the index were AAPL (6.1%), MSFT (5.8%), AMZN (3.9%), FB (2.2%), GOOGL (2.2%), GOOG (2.1%), TSLA (1.7%), BRK.B (1.4%), NVDA (1.4%), JPM (1.3%), and JNJ (1.2%). The remaining stocks represent the rest of the 494 companies in the S&P 500. Guide to the Markets – U.S. Data are as of September 30, 2021.

U.S. Stocks Have Enjoyed Long Run Of Leadership Source:. Goldman Sachs, Factset.

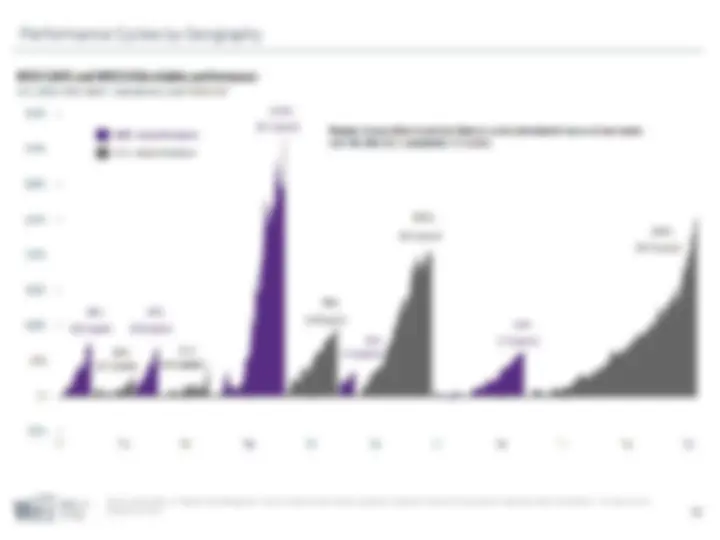

Performance Cycles by Geography Source: FactSet, MSCI, J.P. Morgan Asset Management. *Cycles of outperformance include a qualitative component to determine turning points in leadership. Guide to the Markets – U.S. Data are as of September 30, 2021.

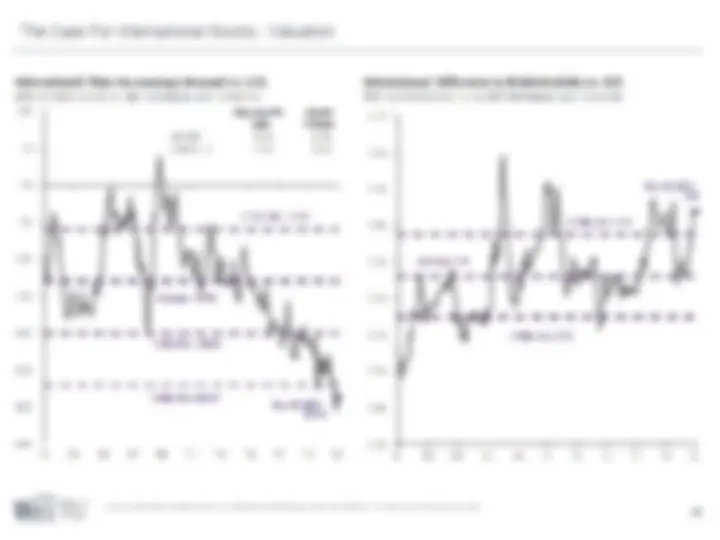

The Case For International Stocks - Valuation Source: FactSet, MSCI, Standard & Poor's, J.P. Morgan Asset Management. Guide to the Markets – U.S. Data are as of September 30, 2021.

10 - Year Asset Class Return Outlook Source: Vanguard Investment Strategy Group.

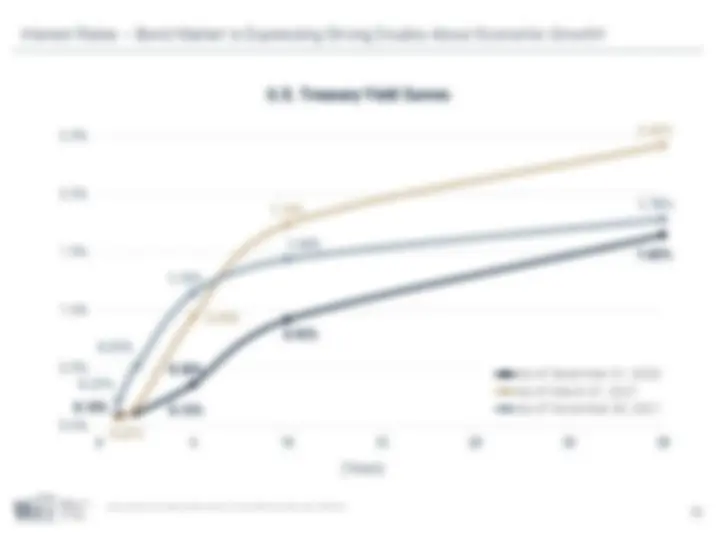

Summary and Game Plan Some of the information enclosed may represent opinions of WST which are subject to change from time to time and which do not constitute a recommendation to purchase and sale any security nor to engage in any particular investment strategy. There are no guarantees investment objectives will be met. Cautious On Short-Term Outlook