13-1

CHAPTER 13

Capital Structure and Leverage

Business vs. financial risk

Optimal capital structure

Operating leverage

Capital structure theory

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Community

Ask the community for help and clear up your study doubts

Discover the best universities in your country according to Docsity users

Free resources

Download our free guides on studying techniques, anxiety management strategies, and thesis advice from Docsity tutors

This PDF is an educational lecture or presentation on Capital Structure, Leverage, and Dividend Policy tailored for academic or professional finance studies. It provides an in-depth overview of key financial concepts, including business and financial risk, operating and financial leverage, optimal capital structure, signaling effects, dividend irrelevance, dividend policies, residual dividends, stock repurchases, and related theories. The content combines theoretical explanations with practical problem-solving exercises, making it a valuable resource for students, researchers, and practitioners interested in corporate finance analysis, optimal capital decision-making, and shareholder distribution strategies.

Typology: Lecture notes

1 / 33

This page cannot be seen from the preview

Don't miss anything!

Probability 0 E(EBIT) EBIT Low risk High risk

What is operating leverage, and how does it affect a firm’s business risk?

Operating leverage is the use of fixed costs rather than variable costs.

If most costs are fixed, hence do not decline when demand falls, then the firm has high operating leverage.

A company’s fixed operating costs are $500,000, its variable costs are $3.00 per unit, and the product’s sales price is $4.00. What is the company’s breakeven point; that is, at what unit sales volume would its income equal its costs? Given: SP = $4/unit; Var. Cost = $3/unit & Fixed =$500, Q BE = Fixed Costs / (Selling Price – Variable Cost) Q BE = $500,000 / ($4.00 - $3.00) Q BE = 500,000 units.

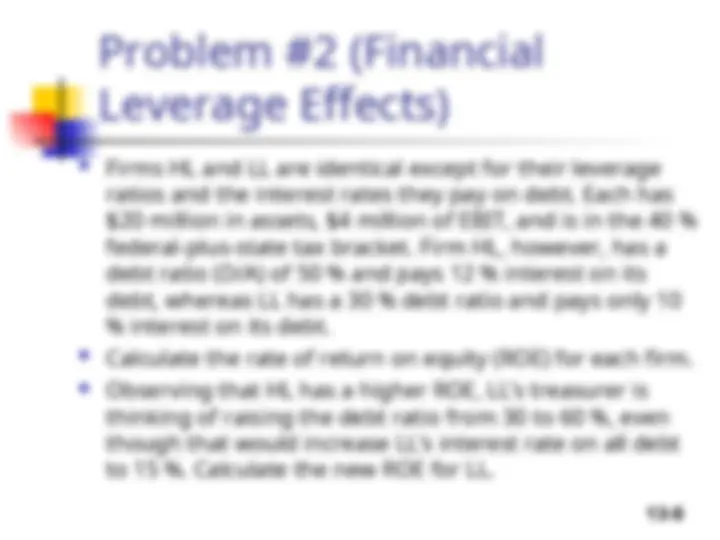

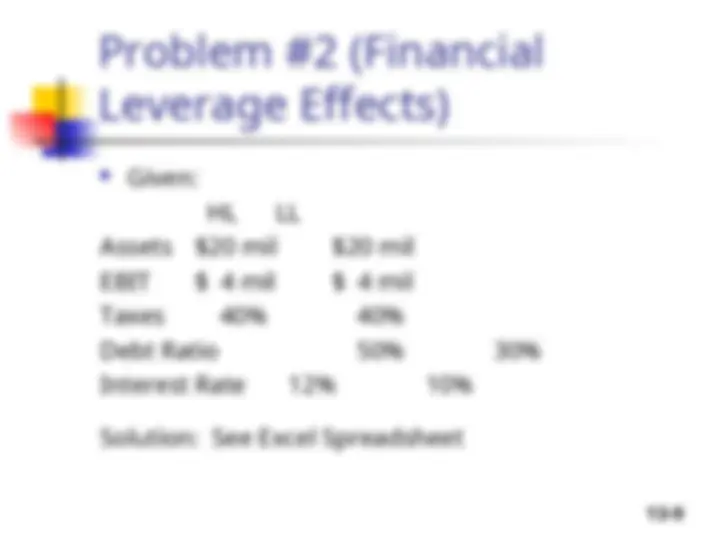

Firms HL and LL are identical except for their leverage ratios and the interest rates they pay on debt. Each has $20 million in assets, $4 million of EBIT, and is in the 40 % federal-plus-state tax bracket. Firm HL, however, has a debt ratio (D/A) of 50 % and pays 12 % interest on its debt, whereas LL has a 30 % debt ratio and pays only 10 % interest on its debt. Calculate the rate of return on equity (ROE) for each firm. (^) Observing that HL has a higher ROE, LL’s treasurer is thinking of raising the debt ratio from 30 to 60 %, even though that would increase LL’s interest rate on all debt to 15 %. Calculate the new ROE for LL.

The effect of leverage on profitability and debt coverage For leverage to raise expected ROE, must have BEP > r d . (^) Why? If r d

BEP, then the interest expense will be higher than the operating income produced by debt-financed assets, so leverage will depress income. As debt increases, TIE decreases because EBIT is unaffected by debt, and interest

expense increases (Int Exp = r d D).

d

Jackson Trucking Company is in the process of setting its tar- get capital structure. The CFO believes the optimal debt ratio is somewhere between 20 and 50 %, and her staff has compiled the following projections for EPS and the stock price at various debt levels: Assuming that the firm uses only debt and common equity, what is Jackson’s optimal capital structure? At what debt ratio is the company’s WACC minimized?

Calculating levered betas and costs of equity If D = $250, b L = 1.0 [ 1 + (0.6)($250/$1,750) ] b L = 1. r s = r RF