Name:

Research Project 3

From the text, the Weighted Average Cost of Capital is:

WACC = (E/V) x RE + (D/V) x RD x (1- TC) (Eq. 14-6)

In this Research Project, the WACC for a selected company will be determined. Fill in the table

to identify your selected company:

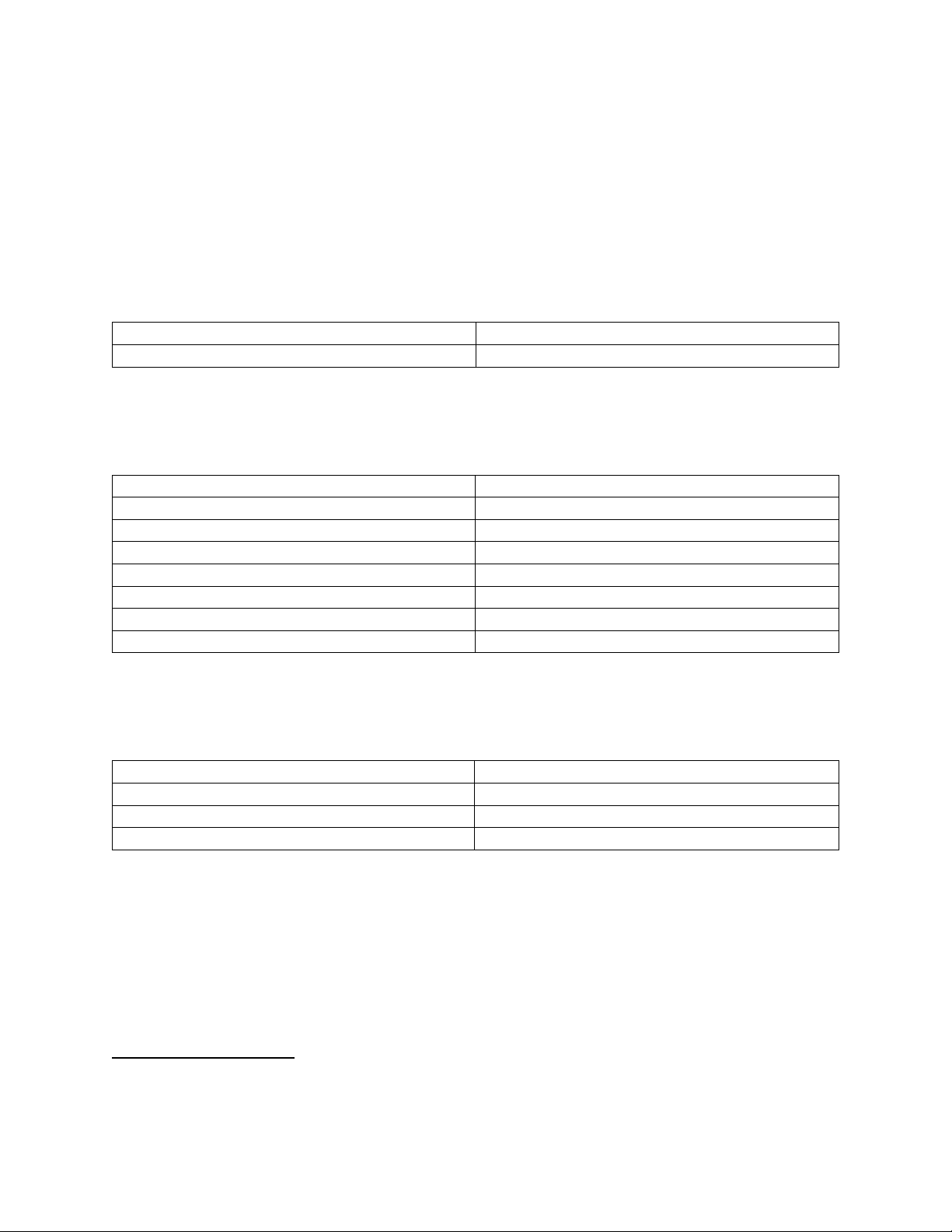

Name of Company/Stock Hershey Company

Ticker Symbol HSY

Part 1: Cost of Debt1

Complete the following table to arrive at the Cost of Debt and Tax Rate.

Interest Income (Expense) – last 2 years avg (127+149)/2= $138,000,000

Earnings Before Tax – last 3 years total 1.797+1.495+1.381= $4,673,000,000

Taxation – last 3 years total 314+22+234= $570,000

Corporate Tax Rate, TC2570,000/4,673,000,000= 0.000121 or 0.012%

Current Debt 942,000,000

LT Debt & Leases 4,087,000,000

Total Debt 942+4087= $5,029,000,000

Cost of Debt3138,000,000/5,029,000,000=0.0274 or 2.74%

Part 2: Cost of Equity and CAPM Components

Complete the table and determine the cost of equity. Show your calculations.

Beta, βE0.45

Historical Market Return, iMAssume 9%

Risk Free Rate, ifAssume 2%

Cost of Equity, iE0.02+(0.45(0.09-0.02))=0.515 or 5.15%

iE=if+βE[E(iM)−if]

1 The inputs from Mergent provide a close approximation to the Cost of Debt

2 Divide the Taxation last 3 years line item by Earnings Before Tax for the last 3 years, as a percent

3 Interest Income (Expense) last 2-year average divided by the Total Debt

1