Download Merlin Group's Financials: Organic Revenue Growth & New Attractions and more Lecture notes Finance in PDF only on Docsity!

Merlin Entertainments plc – 2019 Interim Results

Performance to date broadly in line with Board expectations

1 August 2019

Merlin Entertainments, Europe’s leading and the world’s second-largest visitor attraction operator, today reports results for

the 26 weeks ended 29 June 2019.

Key highlights

26 weeks

ended

29 June

26 weeks

ended

30 June

(restated)

Organic

growth

(constant

currency) (2)

Reported

growth

(actual

currency)

Visitors (1)^ (m) 30.8 29.9 3.0%

Revenue (£m) 763 706 6.5% 8.1%

Underlying EBITDA (£m) 191 188 (0.8)% 1.4%

Underlying operating profit (£m) 79 88 (14.2)% (10.8)%

Underlying profit before tax (£m) 34 43 (21.6)%

Underlying profit for the period (£m) 25 33 (24.4)%

Adjusted earnings per share (p) 2.5 3.3 (24.7)%

Dividend per share (p) - 2.5 n/a

Operating free cash flow (£m) 110 107 2.4%

- During the period the Group adopted IFRS 16, the new accounting standard for leasing. The 2018 results have therefore been restated compared

to previously reported figures to be on an IFRS 16 basis.

- During the period the Group disposed of its two Australian ski resorts. These have been accounted for as discontinued operations in both periods

and accordingly the results above relate to the continuing operations of the Group excluding the ski fields.

- To aid understanding of these items, a reconciliation to previously reported numbers is shown on page 12.

Summary

- Group organic revenue grew by 6.5%, driven by like for like revenue growth of 2.3% as Midway Attractions and Resort

Theme Parks return to growth, and the continued roll out of new attractions and accommodation;

- Midway Attractions organic revenue grew by 8.1%, with a steady recovery in London trading and growth elsewhere;

- Resort Theme Parks organic revenue growth of 4.1% driven by product investment, accommodation openings and

favourable trading at Easter;

- LEGOLAND Parks organic revenue increased by 4.6% with continued accommodation openings offsetting challenging

trading in the existing estate;

- Accommodation revenue grew by 14.5% on a constant currency basis and now represents 24% of theme park revenue;

- Significant cost pressures, partially mitigated by the Productivity Agenda, have limited EBITDA growth;

- Increased depreciation charge relating to the significant investment in the business, and an increased tax charge due to US

legislation, combined with the operating performance, resulted in a 24.7% decline in adjusted earnings per share;

- Improved cash generation, with operating free cash flow of £110 million, representing growth of 2.4%;

- No dividend proposed, following the 28 June announcement regarding the Recommended Offer;

- Continued focus upon long term investment opportunities, with progress against the opening of new LEGOLAND parks

and roll out of new brands.

Nick Varney, Chief Executive Officer, said:

“Group performance year to date has been broadly in line with our expectations in the seasonally quieter first half of the

year, with 6.5% organic revenue growth driven by a combination of like for like growth, continued contribution from new

openings and the benefit of a diversified portfolio.

After a number of years of headwinds, it is pleasing to see both Midway and Resort Theme Parks (RTP) returning to better

levels of like for like revenue growth, with improved cash generation. In Midway, we have seen an improvement in London

trading and a generally solid performance elsewhere driving 4.5% like for like revenue growth, whilst RTP has delivered like

for like growth of 3.0% despite difficult comparatives. Trading in LEGOLAND Parks has however been more disappointing.

Although we enjoyed a strong Easter and Spring Break performance, trading since then has been affected by poor weather in

May and June, difficult market conditions in a number of countries and limited momentum from ‘The LEGO Movie 2’.

With eight new Midway attractions opened in the period, 372 new accommodation rooms, and the ongoing development of

new LEGOLAND parks, we continue to build on our position as a unique, multi-format international operator of strongly

branded and IP-led location based entertainment.”

Delivering on the strategy

The Group has made further progress against its strategic growth drivers so far in 2019, and has also expanded and

diversified its portfolio:

Growing the existing estate through planned investment cycles

- Compelling new propositions opened across the estate, including:

o Midway Attractions – ’Broadway’ experience at Madame Tussauds New York and ‘Penguin Ice Adventure’ at

SEA LIFE Bangkok Ocean World

o LEGOLAND Parks – ‘The LEGO Movie World’ at LEGOLAND Florida and ‘The Haunted House Monster

Party’ at LEGOLAND Windsor

o Resort Theme Parks – ‘Colossos’ roller coaster at Heide Park.

Exploiting strategic synergies

- Productivity Agenda on track to deliver £35 million of efficiency savings by 2022

o UK-based finance Shared Service Centre to open next month

o A number of central functions rationalised

o Continued pilot of ‘lean’ practices in our theme parks

- Successful launch of Merlin Monthly Membership programme, now accounting for approximately 30% of all UK-wide

Pass sales.

Transforming our theme parks into destination resorts

- Total of 372 new rooms planned for 2019 now open, comprising:

o 142 room Castle Hotel at LEGOLAND Billund Resort

o 128 room Magic Hotel at Gardaland Resort

o 102 ‘Stargazing Pods’ at Alton Towers Resort.

Rolling out new Midway attractions

- Eight new Midway attractions opened to date, including two pilots of the new Peppa Pig World of Play in the US, and a

Dungeon within Alton Towers Resort

- SEA LIFE San Antonio scheduled to open towards the end of 2019.

New LEGOLAND park developments

- Continue to target a 2020 opening for LEGOLAND New York, although timetable and cost are under pressure given

the scale and complexity of the project

o Accommodation is now expected to open in 2021

About Merlin Entertainments plc

Merlin Entertainments plc is a global leader in location based, family entertainment. As Europe's Number 1 and the world's

second-largest visitor attraction operator, Merlin now operates over 130 attractions, 20 hotels and 6 holiday villages in 25

countries and across 4 continents. Merlin’s purpose is to deliver memorable experiences to 67 million guests around the

world, through its iconic global and local brands, and the commitment and passion of its c.28,000 employees (peak season).

The Company invests in the development of outstanding visitor experiences across multiple formats, and consistently

achieves above 90% guest satisfaction levels.

It is headquartered in Poole, Dorset, UK and is listed on the London Stock Exchange (MERL.L). In 2018, Merlin had revenues

of £1.7 billion and underlying EBITDA of £494 million. Reflecting its longstanding strategy of diversification and global

expansion, Merlin generates over 70% of profits from outside of the UK.

Merlin’s strategy since its inception in 1999 has been to create a high growth, high return family entertainment company

based upon strong brands and a global portfolio that is naturally balanced against the impact of external factors. It operates

two distinct products – Midway attractions and theme parks.

‘Midway’ attractions are high quality, branded, indoor attractions, with a typical 1-2 hour dwell time, located in city centres,

shopping malls or resorts. There are approximately 120 Midway attractions across 22 countries, with chainable brands

including SEA LIFE, Madame Tussauds, The Eye (observation attractions), The Dungeons and LEGOLAND Discovery

Centres. Midway also incorporates the Little BIG City brand which has attractions in Berlin and Beijing, and two new brand

concepts: The Bear Grylls Adventure which opened its first attraction last year in Birmingham, UK, and Peppa Pig World of

Play, a pre-school play experience with initial roll out in China and the US.

Merlin’s theme parks are larger multi-day outdoor resort destinations, incorporating on-site themed accommodation. These

are organised into two specific Operating Groups, based on the brands.

- LEGOLAND Parks – Eight LEGO themed interactive theme parks appealing to younger families with children aged

2-12. The LEGOLAND Parks estate spans seven countries across three continents, with plans already announced

for further parks in New York, US and South Korea and discussions ongoing regarding parks in China.

- Resort Theme Parks – Six nationally recognised destination theme parks arranged around a central theme. Resort

Theme Parks include Alton Towers, THORPE PARK, Chessington World of Adventures, Warwick Castle in the UK,

and Gardaland (Italy) and Heide Park (Northern Germany).

The trend towards shorter, more frequent breaks has supported the growth of Merlin’s themed on-site accommodation

within its theme parks. Merlin has c.4,500 rooms across a variety of accommodation formats and price points, including four-

star hotels, lodges and glamping.

Merlin delivers safe, memorable experiences every day for its guests through its own brands or, increasingly, through

exclusive partnerships with Intellectual Property owners. It is supported by its unique internal department – Merlin Magic

Making – providing development, creative, production and project management expertise.

Merlin is committed to being a force for good, aiming to make a difference to the communities linked to its business. Merlin’s

Magic Wand (www.merlinsmagicwand.org) is a charity which supports children facing challenges of serious illness, disability

or adversity to experience the magic of Merlin’s attractions, and SEA LIFE Trust (www.sealifetrust.org), promotes and

contributes to marine conservation around the world.

See Merlin Backstage (www.backstage.merlinentertainments.biz or www.facebook.com/merlinbackstage) for an insight into

how Merlin delivers memorable experiences to its many millions of visitors to its attractions.

Visit www.merlinentertainments.biz for more information and follow on Twitter @MerlinEntsNews.

Number of attractions

Movement in the number of attractions between 29 December 2018 and 29 June 2019:

UK Cont. Europe Americas Asia Pacific Total

29 Dec 2018

Mov’t

29 Jun 2019

29 Dec 2018

Mov’t

29 Jun 2019

29 Dec 2018

Mov’t

29 Jun 2019

29 Dec 2018

Mov’t

29 Jun 2019

29 Dec 2018

Mov’t

29 Jun 2019

SEA LIFE 11 -^11 18 -^18 8 -^8 9 2 11 46 2

MT (1)^^2 -^2 4 -^4 7 -^7 10 -^10 23 -^23

Dungeons 5 1 6 3 -^3 1 -^1 1 -^1 10 1

LDC (2)^^2 -^2 3 -^3 11 1 12 4 2 6 20 3

Eye 2 -^2 -^ -^ -^ -^ -^ -^1 -^1 3 -^3

Other 2 -^2 1 -^1 -^2 2 8 (2)^6 11 -^11

Midway(3)^24 1 25 29 -^29 27 3 30 33 2 35 113 6

LLP (4)^1 -^1 2 -^2 2 -^2 3 -^3 8 -^8

RTP (5)^4 -^4 2 -^2 -^ -^ -^ -^ -^ -^6 -^6

Group 29 1 30 33 - 33 29 3 32 36 2 38 127 6 133

Note: (1) (^) Madame Tussauds (2) (^) LEGOLAND Discovery Centre (3) (^) Midway Attractions Operating Group (4) (^) LEGOLAND Parks Operating Group (5) (^) Resort Theme Parks Operating Group

Attractions opened to date in 2019 comprise Alton Towers Dungeon; LDC Beijing, San Antonio and Shenyang; SLC Malaysia and Shenyang and Peppa Pig World of Play in Dallas and Michigan. Attractions sold in the period comprise the two ski fields in Australia.

Number of rooms

Movement in the number of accommodation rooms between 29 December 2018 and 29 June 2019:

29-Dec-18 Rooms opened Other movements 29-Jun-

Billund (Denmark) 436 142 - 578

Windsor (UK) 209 - - 209

California 500 - - 500

Deutschland 461 - - 461

Florida 318 - - 318

Malaysia 263 - - 263

Dubai - - - -

Japan 252 - - 252

LEGOLAND Parks 2,439 142 - 2,

Alton Towers (UK) 592 102 - 694 Chessington World of Adventures (UK) 254 -^ -^254 Gardaland (Italy) 347 128 - 475

Heide Park (Germany) 329 - - 329

THORPE PARK (UK) 90 - - 90

Warwick Castle (UK) 67 - - 67

Resort Theme Parks 1,679 230 - 1,

Group 4,118 372 - 4,

Note: Excludes campsite pitches at LEGOLAND Deutschland and LEGOLAND Billund.

Operating Group Review

Midway Attractions

£million 26 weeks

ended

29 June

26 weeks

ended

30 June

(restated)

Organic

growth

(constant

currency)

Reported

growth

(actual

currency)

Like for like

growth

Revenue 324 297 8.1% 8.9% 4.5%

Underlying EBITDA 108 107 (0.1)% 0.6%

Underlying operating profit 56 62 (9.7)% (9.2)%

Organic revenue grew by 8.1% in the Midway Attractions Operating Group reflecting like for like growth of 4.5% and the

positive contribution from New Business Development.

Trading in London, the largest of our five regional Divisions has, as anticipated, continued to improve. The business has

grown steadily in the first half of 2019, benefiting from stronger inbound tourism as it recovers following the terrorist attacks

of 2017, and as a result of the weaker Sterling. The Operating Group’s like for like performance was also impacted by the re-

opening of the LEGOLAND Discovery Centre in Shanghai, following its temporary closure last year. Finally, the adverse

effect on visitation of the removal of the beluga whales from Chang Feng Ocean World in Shanghai has been significant for

the site, but consistent with previous expectations. Elsewhere across the Midway portfolio, revenue growth has been solid.

Our Midway roll out programme contributed an additional £14 million revenue in the period (of which £1 million related to

SEA LIFE Nagoya which is included in the LEGOLAND Parks result), with new brands or openings in new markets

representing approximately half of this.

Underlying EBITDA was broadly flat on a constant currency basis. The margin declined however from 36.0% to 33.2% partly

as a result of the ongoing cost pressures in the existing estate, but primarily due to the significant investment in openings of

new brands or attractions in new markets. These attractions typically have lower rates of return at the outset as they

establish themselves, contributing revenue, but limited profit.

The small increase in EBITDA, combined with growth in depreciation driven by continued investment in the existing estate,

Productivity Agenda and New Business Development, resulted in a decline in operating profit of £6 million (9.7% at constant

currency).

LEGOLAND Parks

£million 26 weeks

ended

29 June

26 weeks

ended

30 June

(restated)

Organic

growth

(constant

currency)

Reported

growth

(actual

currency)

Like for like

growth

Revenue 296 274 4.6% 7.9% (0.7)%

Underlying EBITDA 91 89 (2.5)% 1.3%

Underlying operating profit 62 65 (9.5)% (5.6)%

Organic revenue grew by 4.6% in the LEGOLAND Parks Operating Group, driven by the continued roll out of new

accommodation offsetting a decline in like for like revenue.

142 accommodation rooms have been added to the LEGOLAND estate with the opening of the Castle Hotel at LEGOLAND

Billund Resort. Total accommodation revenue grew by 19.6% on a constant currency basis to represent 25% of LEGOLAND

Parks revenue (2018: 22%).

Like for like revenue declined by 0.7%. Although the Operating Group delivered a strong Easter and Spring Break

performance, trading since then has been more challenging due to poor weather and difficult trading conditions in a number

of markets. Additionally, whilst our new ‘The LEGO Movie World’ land at LEGOLAND Florida has enjoyed favourable guest

feedback, there has otherwise been limited trading momentum as a result of the film itself. Nevertheless, we continue to

enjoy levels of Guest Satisfaction in excess of 90%, and have further improved our ‘Top Box’ measure.

Underlying EBITDA declined by 2.5% on a constant currency basis, representing a margin decline from 32.7% to 30.7%. This

is the result of the decline in like for like revenue, continued cost pressures and, to a lesser extent, increasing pre-opening

costs related to LEGOLAND New York.

Operating profit declined by 9.5% on a constant currency basis due to the decline in EBITDA and increased depreciation

associated primarily with the continued investment in accommodation.

Resort Theme Parks

£million 26 weeks

ended

29 June

26 weeks

ended

30 June

(restated)

Organic

growth

(constant

currency)

Reported

growth

(actual

currency)

Like for like

growth

Revenue 137 133 4.1% 3.6% 3.0%

Underlying EBITDA 16 15 9.7% 9.8%

Underlying operating profit (9) (10) 5.9% 7.0%

Organic revenue grew by 4.1% in the Resort Theme Parks Operating Group, reflecting like for like revenue growth of 3.0%

and the contribution from new accommodation.

230 rooms were opened during the period comprising the 128 room Magic Hotel at Gardaland Resort, and 102 ‘Stargazing

Pods’ at Alton Towers Resort. Total accommodation revenue grew by 3.8% on a constant currency basis to represent 21%

of revenue (2018: 21%).

The good like for like performance, despite challenging comparatives, is a result of product initiatives such as ‘Room on the

Broom’ at Chessington World of Adventures and the relaunch of ‘Colossos’ at Heide Park together with favourable Easter

weather in the UK.

As a result of the revenue growth, underlying EBITDA improved slightly and the seasonal operating loss narrowed to

£9 million.

Taxation

The underlying tax charge on profit before taxation for the 26 weeks ended 29 June 2019 is based on management’s best

estimate of the full year effective tax rate for continuing operations of 25.5% (26 weeks ended 30 June 2018: 22.8%; 52 weeks

ended 29 December 2018: 18.4%). The 2018 full year ETR of 18.4% reflected the one-off impact of prior year adjustments

following changes to US tax legislation. Without that impact, the rate would have been 23.0%. The increase for the 26 weeks

ended 29 June 2019 is primarily due to further refinement of US legislative changes.

Significant factors which may impact the Group’s future effective tax rate include the USA tax reforms, the ability to continue

with our current financing arrangements and changes to local or international tax laws.

Foreign exchange rate sensitivity

Merlin’s income statement is exposed to fluctuations in foreign currency exchange rates principally on the translation of our

non-Sterling earnings. The tables below show the impact on 2019 revenues and EBITDA of re-translating them at 2018

foreign exchange (FX) rates. The seasonality of the Group results in a bias towards non-European earnings in the first half of

the year.

Currency

H1 2019

average FX rates

H1 2018

average FX rates

%age movement in FX rates

Revenue impact £m

USD 1.30 1.37 (5.2)% (13)

EUR 1.15 1.14 1.3% 2

AUD 1.84 1.77 3.6% 1

Other (1)

Change in 2019 revenues at 2018 FX rates (11)

Note: Weighted-average FX rates

Currency

H1 2019

average FX rates

H1 2018

average FX rates

%age movement in FX rates

EBITDA

impact £m

USD 1.30 1.37 (5.0)% (4)

EUR 1.16 1.14 1.2% -

AUD 1.83 1.74 5.4% -

Other -

Change in 2019 EBITDA at 2018 FX rates (4)

Note: Weighted-average FX rates

Earnings per share (EPS)

Basic earnings per share was 2.4p ( 2018: 3.3p).

Adjusted earnings per share, which excludes the impact of exceptional items, was 2.5p ( 2018: 3.3p).

26 weeks ended 29 June 2019 £m

26 weeks ended 30 June 2018 (restated) £m

Underlying profit attributable to shareholders from continuing operations 25 33

Weighted average number of shares (million) 1,023 1,

Adjusted earnings per share (p) 2.5p 3.3p

Dividend

Following the announcement made on 28 June regarding the Recommended Offer for the Company, the Board is not

recommending an interim dividend payment.

Cash flow

26 weeks ended 29 June 2019 £m

26 weeks ended 30 June 2018 (restated) £m

EBITDA 191 188

Exceptional items (2) -

Working capital and other movements 52 76

Tax paid (33) (22)

Cash flow from operating activities 208 242

Capital expenditure (162) (190)

Disposal of subsidiaries 92 -

Net proceeds from/(repayment of) borrowings 20 (125)

Capital repayment of lease liabilities (22) (18)

Interest paid, net of interest received (51) (49)

Refinancing and other costs (1) (1)

Dividend paid (56) (51)

Other 2 3

Net cash inflow/(outflow) for the period 30 (189)

Merlin continues to be cash generative, delivering operating free cash flow (being EBITDA less existing estate capital

expenditure) of £110 million in the period (2018: £107 million).

The Group invested £162 million (2018: £190 million) in capital projects during the period, including £81 million in the

existing estate and £81 million on New Business Development. 2019 capex is now likely to be slightly below that previously

guided, in part due to accommodation at LEGOLAND New York which is now expected to open in 2021. Disposals of

subsidiaries totalled £92 million in respect of the Australian ski fields transaction that completed in April.

The Group’s proceeds from borrowings of £20 million (2018: £125 million outflow) reflect net drawdowns in the period under

the Group’s revolving credit facility. In 2018 the outflow included repayments of term loans as part of the refinancing in April

of that year.

Net debt

June 2019 £m

Dec 2018 (restated) £m

June 2018 (restated) £m

Interest-bearing loans and borrowings 1,120 1,100 1,

Less: cash and cash equivalents (134) (110) (117)

Lease liabilities 1,177 1,183 1,

Net debt 2,163 2,173 2,

Net debt decreased by £10 million from the year end as a result of the cash generation in the period, partly offset by the

adverse impact of foreign exchange movements and movements in lease liabilities. Following the refinancing that took place in

2018, in April we extended the maturity of the Revolving Credit Facility by a further year to 2024.

Restatement of 2018 full year results

The transition to IFRS 16 and the presentation of discontinued operations resulted in the restatement of the income

statement for the 52 weeks ended 29 December 2018 as follows:

£ millions (unless stated) December 2018 (reported) IFRS 16

Discontinued operations

December 2018 (restated)

Revenue 1,688 - (35) 1,

Underlying EBITDA 494 84 (12) 566

Underlying operating profit 327 39 (9) 357

Underlying profit before tax 289 (13) (8) 268

Underlying profit for the period 234 (10) (5) 219

Adjusted EPS (p) 22.9 (1.0) (0.5) 21.

Operating free cash flow 345 84 (7) 422

£ millions (unless stated) December 2018 (reported) IFRS 16

Discontinued operations

December 2018 (restated)

Midway Attractions 210 48 (12) 246

LEGOLAND Parks 242 6 - 248

Resort Theme Parks 88 29 - 117

Central (46) 1 - (45)

Group EBITDA 494 84 (12) 566

Midway Attractions 139 22 (9) 152

LEGOLAND Parks 194 2 - 196

Resort Theme Parks 51 15 - 66

Central (57) - - (57)

Group Operating Profit 327 39 (9) 357

CONDENSED CONSOLIDATED

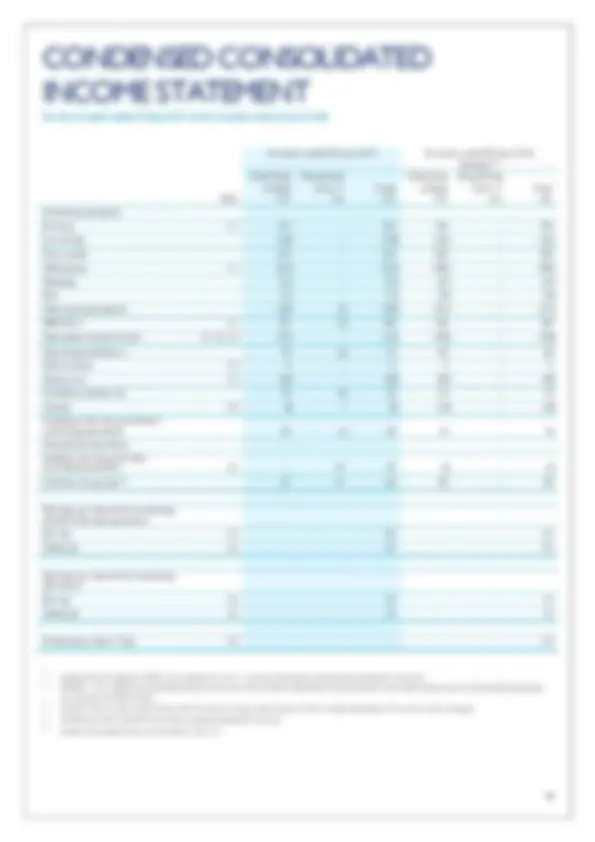

INCOME STATEMENT

For the 26 weeks ended 29 June 2019 (2018: 26 weeks ended 30 June 2018)

26 weeks ended 29 June 2019 26 weeks ended 30 June 2018 Restated (1) Underlying Exceptional Underlying Exceptional trading items (5)^ Total trading items (5)^ Total Note £m £m £m £m £m £m

Continuing operations

Revenue 2.1 763 - 763 706 - 706

Cost of sales (139) - (139) (126) - (126)

Gross profit 624 - 624 580 - 580

Staff expenses 2.1 (223) - (223) (208) - (208)

Marketing (51) - (51) (47) - (47)

Rent (11) - (11) (10) - (10)

Other operating expenses (148) (2) (150) (127) - (127)

EBITDA (2)^ 2.1 191 (2) 189 188 - 188

Depreciation and amortisation 3.1, 3.2, 3.3 (112) - (112) (100) - (100)

Operating profit/(loss) 79 (2) 77 88 - 88

Finance income 2.3 5 - 5 5 - 5

Finance costs 2.3 (50) - (50) (50) - (50)

Profit/(loss) before tax 34 (2) 32 43 - 43

Taxation 2.4 (9) 1 (8) (10) - (10)

Profit/(loss) for the period from continuing operations 25 (1) 24 33 - 33

Discontinued operations

Profit/(loss) for the period from discontinued operations 2.5 - 42 42 (5) - (5)

Profit for the period (3)^25 41 66 28 - 28

Earnings per share from continuing and discontinued operations

Basic (p) 2.6 6.5 2.

Diluted (p) 2.6 6.5 2.

Earnings per share from continuing operations

Basic (p) 2.6 2.4 3.

Diluted (p) 2.6 2.4 3.

Dividend per share (4)^ (p) 4.2 - 2.

( 1 ) Restated for the adoption of IFRS 16 as explained in note 1.1 and the presentation of discontinued operations (note 2.5). ( 2 ) (^) EBITDA – this is defined as profit before finance income and costs, taxation, depreciation and amortisation and is after taking account of attributable profit after

tax of jointly controlled entities. (3) Profit for the 26 weeks ended 29 June 2019 and the 26 weeks ended 30 June 2018 is wholly attributable to the owners of the Company. (4) Dividend per share represents the interim proposed dividend for the year. (5) Details of exceptional items are provided in note 2.2.

CONDENSED CONSOLIDATED

STATEMENT OF FINANCIAL POSITION

At 29 June 2019 (2018: 29 December 2018, 30 June 2018)

29 June 29 December 30 June 30 December 2019 2018 2018 2017 Restated (1)^ Restated (1)^ Restated (1) Note £m £m £m £m

Non-current assets

Property, plant and equipment 3.1 2,206 2,169 2,046 1,

Right-of-use assets 3.2 987 993 968 966

Goodwill and intangible assets 3.3 1,024 1,028 1,017 1,

Investments 5.1 65 61 60 59

Derivative financial assets 8 - - -

Other receivables 13 14 13 11

Deferred tax assets 65 68 63 63

4,368 4,333 4,167 4,

Current assets

Inventories 61 47 52 37

Trade and other receivables 167 122 139 97

Derivative financial assets 3 3 2 5

Cash and cash equivalents 4.1 134 110 117 309

365 282 310 448

Total assets 4,733 4,615 4,477 4,

Current liabilities

Interest-bearing loans and borrowings 4.1 8 8 9 7

Lease liabilities 4.1 38 38 38 33

Derivative financial liabilities 1 4 - 3

Trade and other payables 442 345 411 298

Tax payable 39 43 25 37

Provisions 7 7 5 5

535 445 488 383

Non-current liabilities

Interest-bearing loans and borrowings 4.1 1,112 1,092 1,148 1,

Lease liabilities 4.1 1,139 1,145 1,112 1,

Other payables 25 26 27 9

Provisions 84 80 72 71

Employee benefits 5 6 6 6

Deferred tax liabilities 178 182 171 171

2,543 2,531 2,536 2,

Total liabilities 3,078 2,976 3,024 3,

Net assets 1,655 1,639 1,453 1,

Issued capital and reserves attributable to owners of the Company 1,650 1,634 1,449 1,

Non-controlling interest 5 5 4 4

Total equity 1,655 1,639 1,453 1,

(1) Restated for the adoption of IFRS 16 as explained in note 1.1.

CONDENSED CONSOLIDATED

STATEMENT OF CHANGES IN EQUITY

For the 26 weeks ended 29 June 2019 (2018: 26 weeks ended 30 June 2018)

Total Non- Share Share Translation Hedging Retained parent controlling Total capital premium reserve reserve earnings equity interest equity Note £m £m £m £m £m £m £m £m

At 31 December 2017 (as previously reported) 10 10 (18) 1 1,560 1,563 4 1,

Adjustment on initial application of IFRS 16 (net of tax) - - (2) - (93) (95) - (95)

At 31 December 2017 (restated) 10 10 (20) 1 1,467 1,468 4 1,

Profit for the period - - - - 28 28 - 28

Other comprehensive income for the period net of income tax - - (5) 1 - (4) - (4)

Total comprehensive income for the period - - (5) 1 28 24 - 24

Shares issued - 3 - - - 3 - 3

Equity dividends 4.2 - - - - (51) (51) - (51)

Equity-settled share-based payments 4.3 - - - - 5 5 - 5

At 30 June 2018 10 13 (25) 2 1,449 1,449 4 1,

Profit for the period - - - - 192 192 - 192

Other comprehensive income for the period net of income tax - - 13 - (1) 12 1 13

Total comprehensive income for the period - - 13 - 191 204 1 205

Shares issued - 3 - - - 3 - 3

Equity dividends - - - - (25) (25) - (25)

Equity-settled share-based payments - - - - 3 3 - 3

At 29 December 2018 10 16 (12) 2 1,618 1,634 5 1,

Profit for the period - - - - 66 66 - 66

Other comprehensive income for the period net of income tax - - (3) (1) 3 (1) - (1)

Total comprehensive income for the period - - (3) (1) 69 65 - 65

Shares issued 4.2 - 2 - - - 2 - 2

Equity dividends 4.2 - - - - (56) (56) - (56)

Equity-settled share-based payments 4.3 - - - - 5 5 - 5

At 29 June 2019 10 18 (15) 1 1,636 1,650 5 1,

SECTION 1

BASIS OF PREPARATION

26 weeks ended 29 June 2019

1.1 BASIS OF PREPARATION

Merlin Entertainments plc (the Company) is a company incorporated in the United Kingdom. The condensed consolidated interim financial

statements as at and for the 26 weeks ended 29 June 2019 (2018: 26 weeks ended 30 June 2018) comprise the Company and its subsidiaries

(together referred to as the Group) and the Group’s interests in jointly controlled entities.

The consolidated financial statements of the Group as at and for the 52 weeks ended 29 December 2018 are available on request from the

Company’s registered office at Link House, 25 West Street, Poole, Dorset, BH15 1LD.

All values are stated in £ million (£m) except where otherwise indicated.

Statement of compliance

These condensed consolidated interim financial statements have been prepared in accordance with the Disclosure and Transparency Rules

of the Financial Conduct Authority and with IAS 34 ‘Interim financial reporting’ as adopted by the EU. They do not include all of the

information required for full annual financial statements, and should be read in conjunction with the consolidated financial statements of the

Group as at and for the 52 weeks ended 29 December 2018.

These interim financial statements are not statutory accounts. The statutory accounts for the 52 weeks ended 29 December 2018 have

been reported on by the Company’s auditors and delivered to the Registrar of Companies. The auditor’s report was (i) unqualified, (ii) did

not include a reference to any matters to which the auditors drew attention by way of emphasis without qualifying their report, and (iii) did

not contain a statement under section 498(2) or (3) of the Companies Act 2006.

Going concern

The Group continues to trade profitably, reporting a profit for the period on continuing operations of £24 million (26 weeks ended 30 June

2018: £33 million) and continues to generate cash with net operating cash inflows of £208 million (26 weeks ended 30 June 2018:

£242 million).

The Group is funded by senior unsecured notes due for repayment in 2022 and 2026 and a multi-currency revolving credit facility maturing

in April 2024. The Group’s forecasts show that it is expected to be able to operate within the terms of these facilities. Further details of

these facilities are provided in note 4.1.

After reviewing the Group’s statement of financial position, available facilities, cash flow forecasts and trading budgets, the Directors believe

the Group to be operationally and financially sound and have a reasonable expectation that the Group has adequate resources to continue

in operational existence for the next 12 months.

The Directors note that the Group is currently the subject of an offer for a cash acquisition by Motion Acquisition Limited, which, if

approved by shareholders and subsequently completed, will be effected by means of a Scheme of Arrangement under Part 26 of the

Companies Act 2006. The Board intends to recommend this offer be accepted (with the exception of Søren Thorup Sørensen who has not

participated in the decision because he is the Chief Executive Officer of KIRKBI Invest A/S, a member of the acquisition consortium).

Having considered the Board’s recommendation to shareholders in relation to the acquisition offer, the Directors have not identified any

information which impacted their assessment of going concern. Accordingly, the Group continues to adopt the going concern basis in

preparing its condensed consolidated interim financial statements.

Significant accounting policies

The accounting policies adopted in the preparation of these condensed consolidated interim financial statements are consistent with the

policies applied by the Group in its consolidated financial statements as at and for the 52 weeks ended 29 December 2018, except for the

adoption as of 30 December 2018 of IFRS 16 ‘Leases’.

SECTION 1

BASIS OF PREPARATION CONTINUED

26 weeks ended 29 June 2019

1.1 BASIS OF PREPARATION CONTINUED

IFRS 16 ‘Leases’

IFRS 16 ‘Leases’ became effective for 2019 reporting periods onwards and introduces a single, on-balance sheet lease accounting model for

lessees.

The Group has considered its entire lease portfolio which substantially relates to land, buildings and infrastructure assets, as follows:

- For leases previously classified as operating leases, the Group has recognised a new asset in the form of a right-of-use (ROU) asset,

together with an associated lease liability. The income statement now includes a depreciation charge for the ROU asset and an interest

expense on the lease liability. This replaces the previous accounting for operating leases that were expensed within operating expenses

on a straight-line basis over the term of the lease. Where the Group’s lease expense is linked to turnover or other performance

criteria, this element continues to be recorded as rent within operating expenses.

- Existing finance leases have also been reviewed against the new standard. As a result a number of leases entered into under historic

sale and leaseback transactions have been re-assessed due to differences in the accounting treatment between IAS 17 and IFRS 16 of

unguaranteed residual values. This has required re-assessment of the values of leased assets at inception and their treatment under

IFRS 16 in subsequent periods. Regarding classification, these assets were accounted for as PPE under IAS 17 but are treated as ROU

assets under IFRS 16.

- The Group has elected to take recognition exemptions for short term leases and leases of low-value items. Leases that fall within the

Group’s defined parameters for these exemptions have been excluded from the IFRS 16 lease accounting requirements and will be

expensed on a straight-line basis over the life of the lease.

Judgements and estimates

IFRS 16 requires certain judgements and estimates to be made. The most significant of these relate to the following:

- The discount rate used in the calculation of the lease liability, which involves estimation. Discount rates are calculated on a lease by

lease basis. For the property leases that make up substantially all of the Group’s lease portfolio this results in two approaches. For a

small volume of high value leases, the rate implicit in the lease can be calculated and is therefore adopted. Otherwise, for the majority

of leases the rate used is based on estimates of incremental borrowing costs. These will depend on the territory of the relevant lease

and hence the currency used; the date of lease inception; and the lease term. As a result, reflecting the breadth of the Group’s lease

portfolio; the transition approach adopted which has required estimation of historic discount rates; and estimations as to lease lives,

there are a large number of discount rates within a wide range.

- IFRS 16 defines the lease term as the non-cancellable period of a lease together with the options to extend or terminate a lease, if the

lessee were reasonably certain to exercise that option. Where a lease includes the option for the Group to extend the lease term, the

Group makes a judgement as to whether it is reasonably certain that the option will be taken. This will take into account the length of

time remaining before the option is exercisable; current trading; future trading forecasts as to the ongoing profitability of the attraction;

and the level and type of planned future capital investment. A small number of large leases held by the Group came into effect as part

of a sale and leaseback transaction that occurred in 2007. These leases have an initial lease period of 35 years, with an option to extend

for two further periods of 35 years, subject to an adjustment to market rates at that time. At this point it is not reasonably certain that

these leases will be renewed, taking into account the factors noted above. This judgement is reassessed at each reporting period. A

reassessment of the remaining life of the lease could result in a recalculation of the lease liability and a material adjustment to the

associated balances.

Transition approach and impact

The Group has applied IFRS 16 from 30 December 2018, using the fully retrospective approach. Therefore, the cumulative effect of

adopting IFRS 16 has been recognised, in line with IAS 8 ‘Accounting policies, changes in accounting estimates and errors’, by restating the

52 week period ended 29 December 2018 and making an opening equity adjustment as at 31 December 2017. The Group is not required

to make any adjustment for leases in which it is a lessor except where it is an intermediate lessor in a sub-lease. The Group has applied the

practical expedient to grandfather the definition of a lease on transition. This means that IFRS 16 has been applied to all contracts entered

into before 30 December 2018 and identified as leases in accordance with IAS 17 and IFRIC 4.

The Group’s leverage threshold loan covenants are under ‘frozen-GAAP’ and as such the adoption of IFRS 16 does not impact the ability to

comply with them.